Introduction

Walmart Inc. stands as one of the most powerful and transformative companies in modern economic history. What began as a single discount store in rural Arkansas has grown into the world’s largest corporation. The everyday shopping habits of hundreds of millions of people is influenced by Walmart.

Illustration 1: The Walmart Spark, a symbol that represents affordability, low prices and accessibility.

Walmart is far more than a place to buy groceries or home goods. It is a global entity operating on a scale that few companies in any industry have ever achieved.

From its headquarters in Bentonville, Arkansas, Walmart oversees thousands of stores. It manages massive distribution networks. Walmart has one of the most sophisticated supply chains on Earth.

The company’s guiding philosophy, known as Everyday Low Prices, revolutionized retail by combining relentless cost discipline with unparalleled operational efficiency.

Traditional retailers expanded cautiously. Meanwhile, Walmart pushed forward with aggressive store openings. It engaged in tight supplier negotiations and made investments in logistics technology. These strategies allowed it to dominate markets across the United States.

Today, Walmart operates e-commerce platforms, digital marketplaces, and financial services. It also manages last-mile delivery systems, robotics labs, and one of the world’s largest private trucking fleets. With its increasing emphasis on data, automation and online retail, Walmart continues to redefine the future.

History

The Walmart story began in 1962 when Sam Walton opened the first Walmart Discount City store in Rogers, Arkansas. His core belief was that customers should have access to quality goods at the lowest possible prices. This philosophy set Walmart apart from competitors at a time when discount stores were seen as low-quality alternatives.

Illustration 2: First Wall Mart opened in Rogers, Arkansas

Walton’s approach quickly attracted loyal shoppers, especially in underserved rural areas where Walmart filled a significant retail gap.

During the 1970s and 1980s, Walmart expanded throughout the American South and Midwest. It built a formidable network of stores. This network was supported by a logistics system. This system would become one of its greatest strengths.

Illustration 3: A classical Walmart Store in Englewood, Colo

When the company introduced Walmart Supercenters, it combined general merchandise with full grocery departments. Walmart then became the dominant grocery retailer in the United States. It holds this position overwhelmingly to this day.

The 1990s marked Walmart’s international expansion, beginning with Mexico and Canada followed by ventures into Asia, South America and Europe. Some markets proved challenging. Yet, Walmart’s global presence remains significant. Millions of customers visit its stores and online platforms every day.

The company’s greatest transformation came in the 2010s and 2020s, when it invested heavily in e-commerce through acquisitions such as Jet.com and Flipkart in India and by building its own digital infrastructure to compete directly with Amazon.

Today, Walmart operates over 10,000 stores across multiple continents, employs more than two million people and consistently ranks among the world’s most influential and valuable companies.

Operations

Global Presence

Walmart’s operations span thousands of physical stores in various formats, including Supercenters, Neighborhood Markets, and Sam’s Club warehouse stores. It also runs a rapidly growing international division with strong presences in Mexico, Central America, India, and other regions.

More than 240 million customers visit Walmart stores and websites every week. They rely on the company for groceries, apparel, electronics, home essentials, pharmaceuticals, and countless other products.

The scale at which Walmart operates is staggering. It handles immense volumes of goods from suppliers around the world, manages advanced transportation systems and depends on real-time data. Its U.S. network is vast. Most Americans live within a short drive of a Walmart. This gives the company a unique advantage.

E-Commerce and Digital Transformation

Although Walmart built its empire through physical retail, the company has undergone a dramatic digital transformation over the past decade. It now operates one of the largest e-commerce platforms in the United States. The company is rapidly expanding in online grocery delivery, general e-commerce and third-party marketplace sales.

Walmart’s membership program, known as Walmart Plus, provides customers with fast delivery. It offers fuel discounts and various digital conveniences. These conveniences integrate online and in-store shopping.

Illustration 4: A automated Walmart distribution center with robo-forklifts. Image gathered from: Robo-Forklifts Rev Up Walmart’s Warehouses

The company is also building automated fulfillment centers inside or adjacent to existing stores. They use robotics and machine learning to improve picking speed and reduce costs. This helps fulfill orders within hours.

Walmart employs thousands of engineers, data scientists and technology specialists. They work on advanced inventory systems, artificial intelligence, cybersecurity and cloud architecture. Its growing network of micro-fulfillment centers shows Walmart’s ambition. The company aims to become a digital and technological powerhouse. It wants to rival the world’s leading tech giants.

Supply Chain Dominance

Walmart’s supply chain is often described as one of the greatest business achievements of the modern era.

The company pioneered real-time inventory tracking, satellite-linked store communication and massive automated distribution hubs long before competitors embraced similar technologies.

Its private truck fleet is among the largest in the world. Walmart’s centralized procurement operations allow them to negotiate favorable terms with suppliers. This often influences manufacturing standards, packaging, and pricing across entire industries.

This logistics mastery allows Walmart to move goods efficiently, reduce waste, and keep prices lower than most competitors. The company’s distribution network connects thousands of suppliers to millions of customers with remarkable speed and accuracy. This connection creates a competitive advantage. It has proven extremely difficult for rivals to replicate.

Illustration 5: A Walmart truck, walmart has one of the largest truck fleets in the world (image gathered from: Walmart Eases Supplier Delivery Demands as Stocking Pressures Recede – WSJ).

Key Competitors

Walmart operates in a highly competitive retail environment, with Amazon as its strongest rival. Amazon leads in e-commerce, cloud services, and digital innovation. In contrast, Walmart excels in physical retail and groceries. This creates an ongoing battle between scale and technology.

Illustration 6: Target is growing competitor (Image from New Target Stores and Facilities).

Target competes by focusing on curated products and a stylish customer experience, appealing to shoppers who value design.

Costco remains a major force through its membership model and strong loyalty, pushing Sam’s Club to keep improving. Traditional grocers like Kroger and Albertsons challenge Walmart on fresh food and store quality. Global retailers such as Carrefour, Aldi, Tesco and Alibaba leverage regional strength. They also use advanced digital tools.

Dollar General and Dollar Tree add pressure at the extreme value end. They are expanding into areas where Walmart’s larger stores don’t fit. Together, these competitors force Walmart to continuously refine pricing, logistics, and its overall shopping experience.

Competitive Advantages

Walmart’s greatest advantage is scale. Its purchasing power and extensive distribution network allow it to secure low costs and maintain everyday low prices.

The company’s supply chain is supported by automation and AI. Real-time inventory systems also play a role. Together, they make it one of the most efficient in the world.

Walmart has a powerful position due to its nationwide store network. It blends physical stores with services like curbside pickup. It also offers same-day delivery. This reach is difficult for online-only competitors to replicate.

Walmart’s financial strength enables sustained investment in technology, store upgrades and new services. Its long-standing reputation for value and convenience continues to build loyalty, especially during economic downturns.

Illustration 7: Walmart has made a bug bed on new technology (image from Walmart is betting big on new technology. But can it deliver where others haven’t? | CNN Business)

Ongoing investments in digital tools and automation ensure Walmart remains competitive. Retail is increasingly shifting toward speed, convenience, and technological integration.

Stock Analysis

In this section we will analyze Walmart’s stock to see if it is a good stock to buy or not. Our philosophy is value investing meaning that we try to find good quality companies that are undervalued. However, we will give a holistic overview. This allows all kinds of investors with different philosophies to judge the stock for themselves.

Revenue and Profits

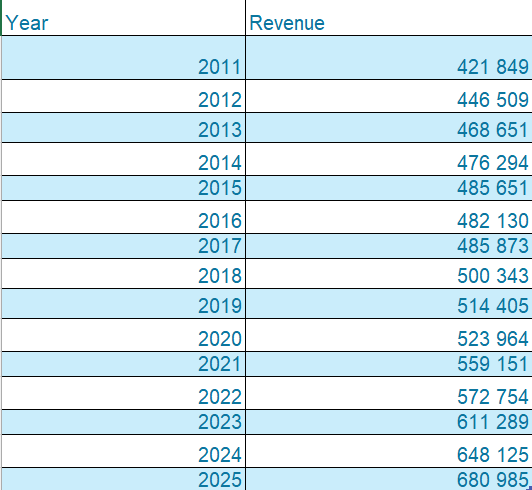

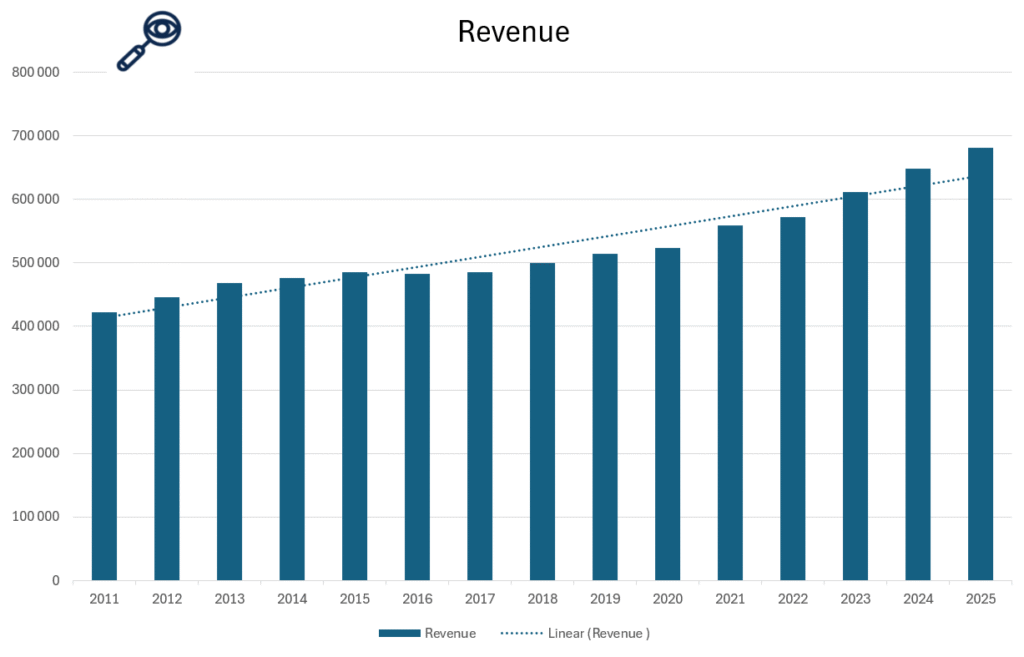

Illustration 8 and 9: Revenue of Walmart from 2011 to 2025

As shown in Illustrations 8 and 9, Walmart has maintained steady revenue growth. It went from around USD 421 billion in 2010 to around 680 billion in 2025. There were no major spikes or declines. This smooth upward trajectory is a strong green flag, indicating that Walmart has a sound business strategy and now how to deliver long-term and not only short-term.

Walmart’s revenue dipped between 2015 and 2016 mainly because a strong U.S. dollar reduced the value of its international sales, even though customers abroad were still spending. At the same time, Walmart closed underperforming stores in markets like Brazil and China, and made major price cuts in the U.S. to stay competitive, which lowered the amount earned per sale.

Overall, Walmart’s financial performance is a green flag for value investors as it shows a company that is stable, has increased its revenue steadily over time and been able to grow and handle crisis.

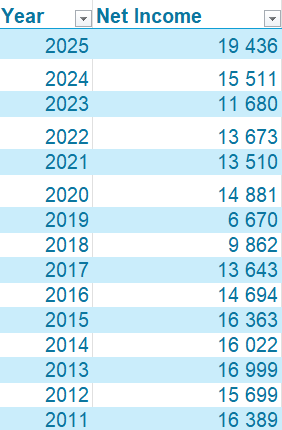

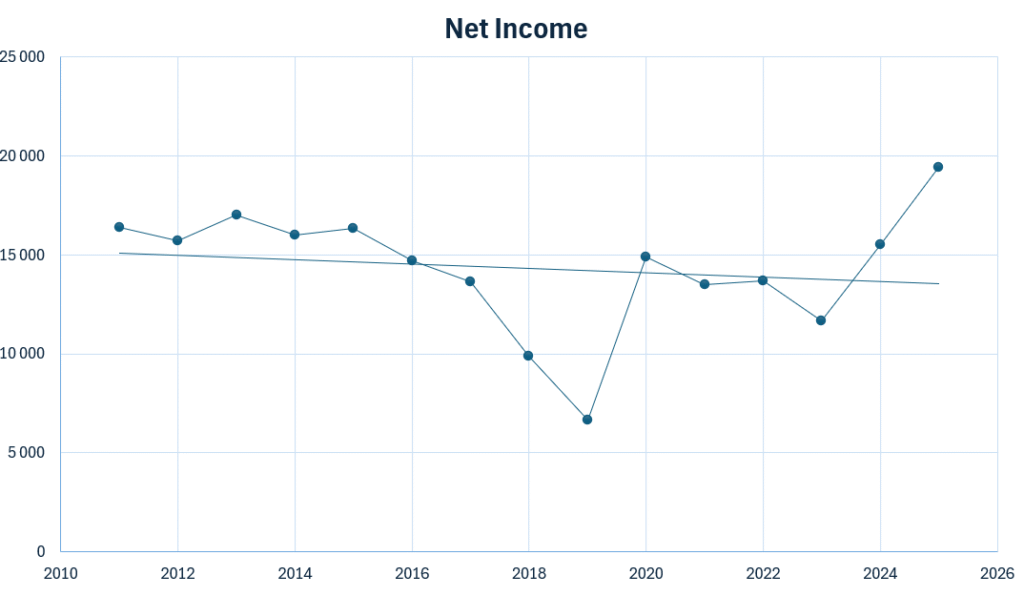

Illustration 10 and 11: Net Income for Walmart from 2011 to 2025

Net income is a crucial metric to evaluate when determining whether a company is a worthwhile investment. It represents a company’s net profit or loss after accounting for all revenues and income items. All expenses are deducted to calculate the net income as Net Income = Revenue – Expenses.

For Walmart, as seen in illustration 10 and 11, the steady decline in net income from 2011 to 2019 and again from 2020 to 2023 is a notable red flag. This decline signals rising operating costs and heavy price cuts to stay competitive. Increased labor and wage expenses have further impacted the margins. Additionally, significant investments in e-commerce and logistics weighed on their margins. These years show that even with strong sales, profitability was under pressure.

However, the renewed growth in net income from 2023 to 2025 is an encouraging development. It demonstrates that Walmart’s efficiency measures are finally boosting earnings again. Supply-chain improvements and a maturing online ecosystem are also strengthening the company’s overall financial outlook.

Overall, the net income of Walmart is a negative sign as it has been a steadily negative trend that showcases the heavy competitive environment Walmart operates in. However, the recent upwards trend from 2023 to 2025 is a good sign.

Revenue Breakdown

![OC] How Walmart makes its Billions: Income statement visualized : r/dataisbeautiful](https://i.redd.it/kzrhc62juoqc1.png)

Illustration 12: Revenue Breakdown for Walmart

As shown in Illustration 12, Walmart U.S. remains the company’s largest revenue driver, consistently generating over 65% of total revenue. This segment includes its core supercenters, neighborhood markets and rapidly expanding e-commerce operations.

Walmart International contributes roughly 20–25% of revenue, driven by operations in Mexico, Canada, China and other key markets. International stores provide meaningful geographic diversification. However, this segment has been sensitive to foreign exchange fluctuations. It also faces competitive pressures and restructuring costs. These factors have occasionally weighed on overall revenue growth.

Sam’s Club, Walmart’s membership-based warehouse chain, accounts for about 10–12% of total revenue. Sam’s Club has shown strong growth in membership fees. Private-label brands and omnichannel offerings also contribute to this growth. These factors help Sam’s Club provide a steady, higher-margin contribution relative to traditional retail sales.

On the cost side, cost of sales typically consumes around 75% of total revenue, reflecting Walmart’s high-volume, low-margin retail model. Operating expenses, including wages, logistics, technology investments, and store operations, take up most of the remainder. These cost pressures help explain Walmart’s historically thin margins and why net income can decline even when revenue remains stable.

Overall, Walmart’s revenue structure reflects a blend of scale, diversification and operational intensity. Walmart U.S. provides consistency. International adds global reach. Sam’s Club offers higher-margin membership growth. Together, these elements create a broad but cost-sensitive revenue foundation for the company.

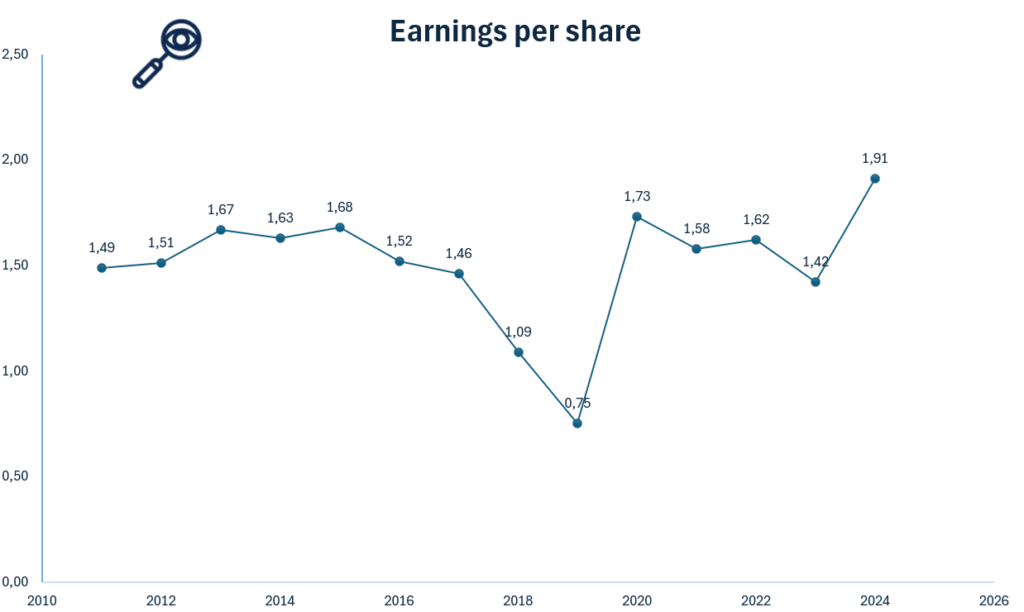

Earnings per Share (EPS)

Illustration 13: Earnings per share (EPS) for Walmart from 2011 to 2025

Earnings Per Share (EPS) is a key financial metric that measures a company’s profitability on a per-share basis. It indicates how much profit a company generates for each outstanding share of its stock. This metric is used to assess a company’s financial health, profitability and potential for growth. In other words this metric can tell us how profitable the business is.

The EPS figure itself isn’t the primary focus for value investors, it can be 0.2 or 10, but what truly matters is the company’s ability to generate consistent earnings growth. A steadily increasing EPS over time signals strong financial health, profitability and long-term value creation.

In Walmart’s case, the decline in EPS from 2013 to 2019 and again from 2020 to 2023 is a clear red flag. This reflects rising wage and operating costs. It also shows price cuts to stay competitive, heavy investments in e-commerce and logistics and weaker performance in several international markets. All of these factors pressured margins and reduced per-share profitability. These periods show that Walmart was spending more to maintain market share while generating less profit per share. However, the renewed EPS increase from 2023 to 2025 is a positive sign. This suggests that its investments in automation, supply-chain efficiency and digital integration are finally paying off. This is encouraging for long-term investors.

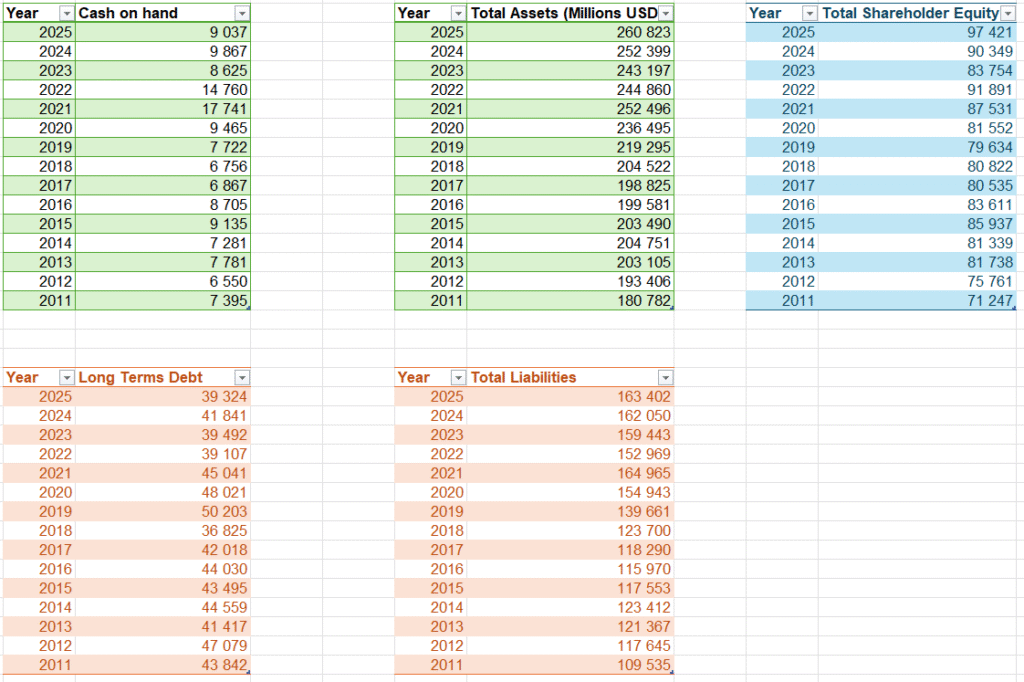

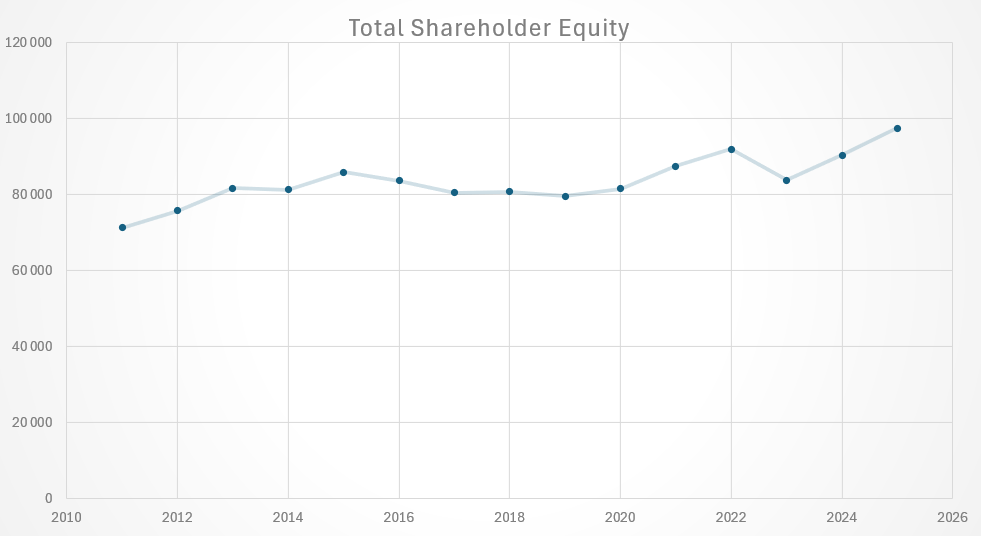

Assets and Liabilities

Illustration 14 and 15: Assets and Liabilities for Walmart from 2011 to 2025

When evaluating a company as a potential investment, understanding its assets and liabilities is crucial. If a local business owner offered to sell their shop to you, one of the first questions, after determining its profitability, would be about its equity and assets. The same principle applies when assessing publicly traded companies like Walmart.

As shown in illustration 14 and 15, Walmart’s total assets have increased steadily from 2011 to 2025 from around 180,7 billion in 2011 to 260,8 in 2025. This trend is a positive sign. However, the flat and sluggish period in asset growth between 2015 and 2020 raises concerns. It indicates several years of limited expansion and investment. This occurred despite rising competition and industry changes.

Walmart’s total liabilities have also grown over time, driven by investments in digital infrastructure, international restructuring and operational modernization. Rising liabilities are not inherently negative. However, they require careful monitoring. This is especially true since Walmart’s cash on hand has declined from 2021 to 2025. It is a worrying sign that reduces financial flexibility. It also limits the company’s ability to absorb shocks or fund large projects without additional borrowing. Cash on hand remains significantly lower than Walmart’s long-term debt. This creates a liquidity imbalance that investors should watch closely.

On a more positive note, total shareholder equity has increased meaningfully from 2011 to 2025. This indicates that Walmart is building value over time. It is also strengthening its financial foundation. This upward trend in equity shows that the company’s asset base is growing faster than its liabilities. This is generally a green flag for long-term financial health. However, the flat period in equity between 2015 and 2020 shows years where Walmart’s financial progress stalled. It highlights the importance of monitoring how effectively future investments translate into real value creation. Overall, Walmart’s balance sheet shows both strengths and caution points. Growing assets and rising equity are positive. However, declining cash levels and high long-term debt require careful attention from investors.

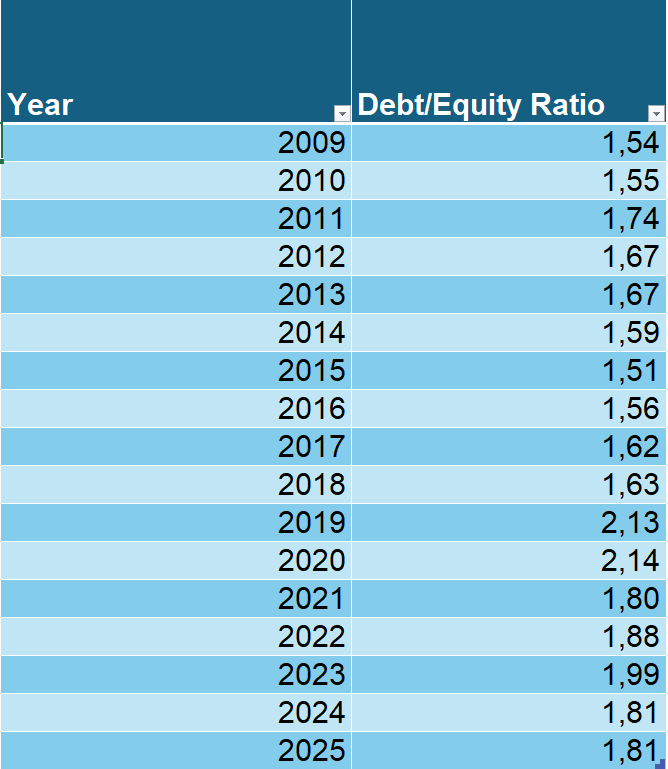

Debt to Equity Ratio

Illustration 16 and 17: Debt to Equity ratio for Walmart from 2009 to 2025

The Debt-to-Equity (D/E) ratio is an important financial metric for assessing a company’s financial leverage and risk. It compares the amount of debt the company uses to finance its operations relative to its shareholder equity. A high D/E ratio suggests that the company relies more heavily on debt to fuel growth, which could increase financial risk, especially during economic downturns when managing debt obligations becomes more challenging. In contrast, a lower D/E ratio indicates that the company is primarily financed through equity, reducing financial risk but potentially limiting its ability to rapidly expand.

Legendary value investor Warren Buffett generally prefers a debt-to-equity (D/E) ratio below 0.5. Walmart’s D/E ratio, however, stood at approximately 1.81 in 2025. Walmart’s D/E ratio has been increasing over time. This is a negative sign as it indicates growing financial leverage and higher reliance on debt to fund operations and investments. That said, the ratio has remained around a relatively stable level, suggesting that while debt is rising Walmart has maintained some balance between borrowing and equity. Investors should monitor this carefully as sustained increases in leverage could pose risks if cash flow or profitability weakens. However, the stability of the ratio over time provides some reassurance that Walmart is managing its debt prudently.

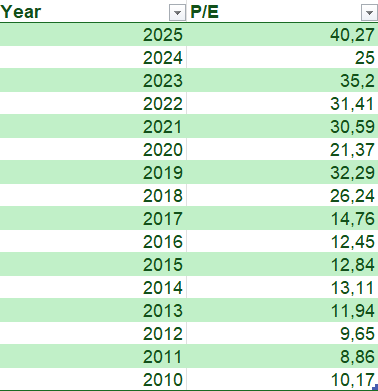

Price to earnings ratio (P/E)

Illustration 18 and 19: P/E Ratio of Walmart from 2010 to 2025

For value investors, one of the most critical metrics when evaluating Walmart’s stock is the price-to-earnings (P/E) ratio, as it helps assess whether the company is undervalued or overvalued. Even if a company has strong financials, purchasing its stock at a high price can lead to poor returns. For example, imagine a business generating solid profits of $1 million per year. If the owner offers to sell you the business for just $1, it would be an incredible deal. But if the owner asks for $1 trillion, even though the business is profitable, the price would be absurdly overvalued. The stock market works similarly, companies can be priced cheaply on some days and excessively expensive on others.

Warren Buffett, a legendary value investor, typically considers stocks with a P/E ratio of 15 or lower as “bargains.” A high P/E ratio suggests that investors are paying a premium for the company’s earnings, expecting significant growth.

Walmart’s P/E has risen sharply over time, it was only 10.17 in 2010, first crossed 20 in 2018, and as of recent years sits around 40.27. This rapid increase suggests that the stock may be significantly overpriced, with investors paying a large premium for Walmart’s earnings based on expectations of growth. Such a high P/E ratio is a cautionary sign for value investors. It indicates that while Walmart is a financially strong and stable company, its current market price may not provide the attractive entry point that lower P/E levels once offered.

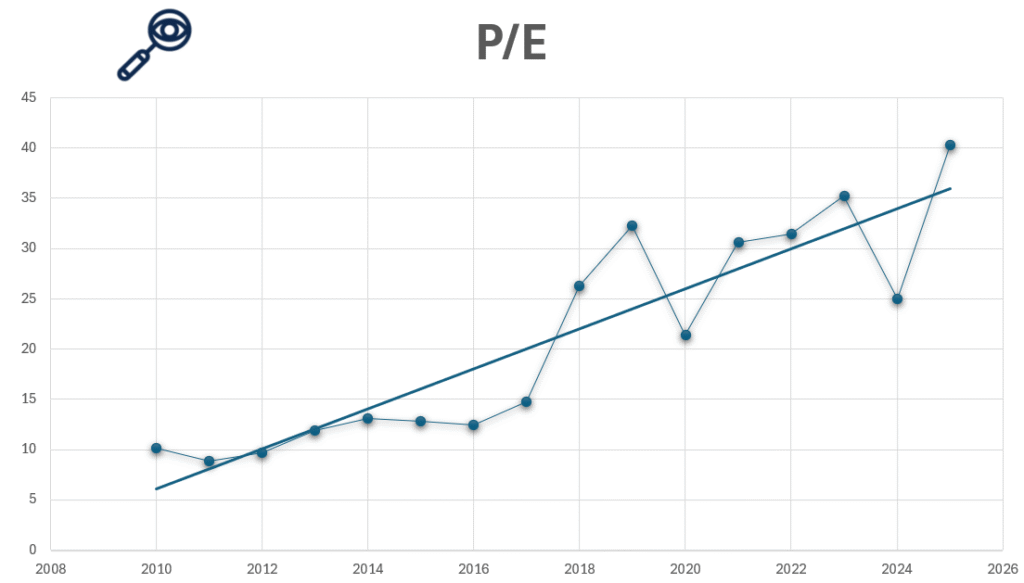

Price to Book Ration (P/B)

Illustration 20 and 21: Price to book ratio for Walmart from 2010 to 2025

Price‑to‑book value (P/B ratio) compares a company’s market valuation (its stock price) to its book value (equity on the balance sheet). A lower P/B ratio suggests that the stock may be undervalued, as investors are paying less for the company’s assets than their actual worth. Conversely, a high P/B ratio may indicate that the stock is overvalued, or that investors expect high growth in the company’s future earnings. The P/B ratio is often used by value investors to assess whether a stock is trading at a fair price based on its underlying assets.

Walmart’s current P/B is very high, standing at 8.85. A P/B that high can be a red flag. It suggests that investors are paying far more than Walmart’s underlying assets are worth in an accounting sense. That could indicate overvaluation. Alternatively, it show a lot of optimism about the stock’s future earnings and cash flow.

Because this valuation is well above the kind of P/B range (e.g., 1–2×) that value investors like Warren Buffett typically favor, it could mean Walmart is less of a classic “bargain value” play today and more a bet on continuing operational strength and competitive positioning.

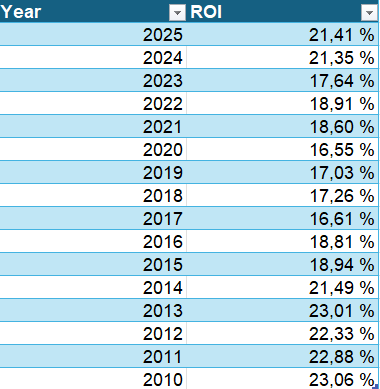

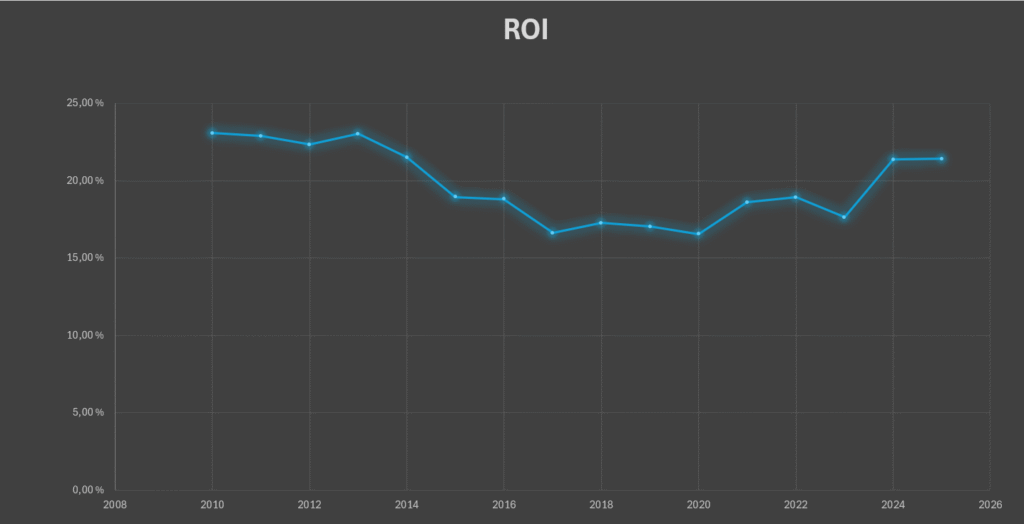

Return on Investment (ROI)

Illustration 22 and 23: Return on investment (ROI) for Walmart from 2010 to 2025

For value investors, Return on Investment (ROI) is a key metric for evaluating Walmart, as it shows how efficiently the company is using its capital to generate profits. A strong ROI indicates that Walmart is generating solid returns relative to the capital it deploys, making it an attractive investment even if the absolute revenue numbers are large.

Historically, Walmart’s ROI has not been bad, hovering around 23% from 2010 to 2013, reflecting the company’s efficient operations and large-scale retail network. However, the steady decline in ROI from 2010 to 2017 is a concerning sign. This decline is largely driven by rising operating costs. Heavy price reductions were made to remain competitive. Significant investments in e-commerce and supply-chain modernization were also made, which temporarily reduced returns on invested capital.

Encouragingly, recent years have seen ROI increase again, signaling that Walmart’s efficiency improvements, digital initiatives and cost-management strategies are paying off. This rebound is a positive indicator for long-term investors. It shows that Walmart is beginning to generate stronger returns on its investments. The company is continuing to expand and modernize its operations.

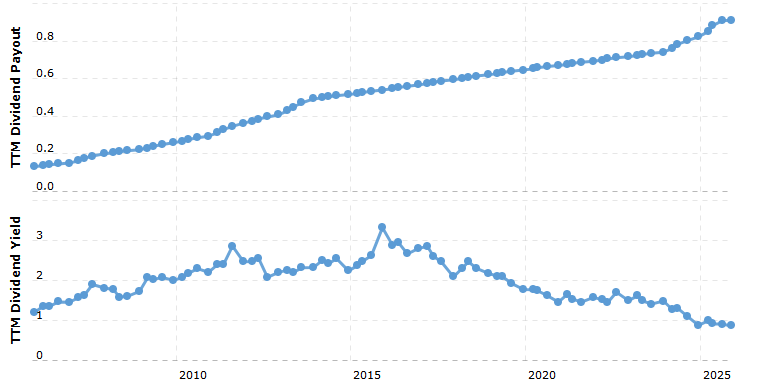

Dividend

Illustration 24: Walmart Dividend Yield and dividend payout ratio from 2005 to 2025.

Walmart currently pays an annual dividend of $0.94 per share, giving it a dividend yield of about 0.89%, which is relatively modest for an income investor. Its payout ratio (the portion of earnings distributed as dividends) hovers around 35%, based on trailing 12 months’ earnings.

From a positive perspective, the low payout ratio is a good sign: Walmart retains a large share of its earnings, supporting its growth efforts and e-commerce investment. That makes the dividend relatively sustainable and not likely to be cut under normal circumstances.

However, there are some cautionary points. The very low yield (below 1%) means that Walmart is not especially attractive purely for dividend income. Investors looking for yield might find other options more compelling. In addition, while Walmart has grown its dividend steadily, a low yield suggests that the market is valuing the stock more for growth potential than for current income.

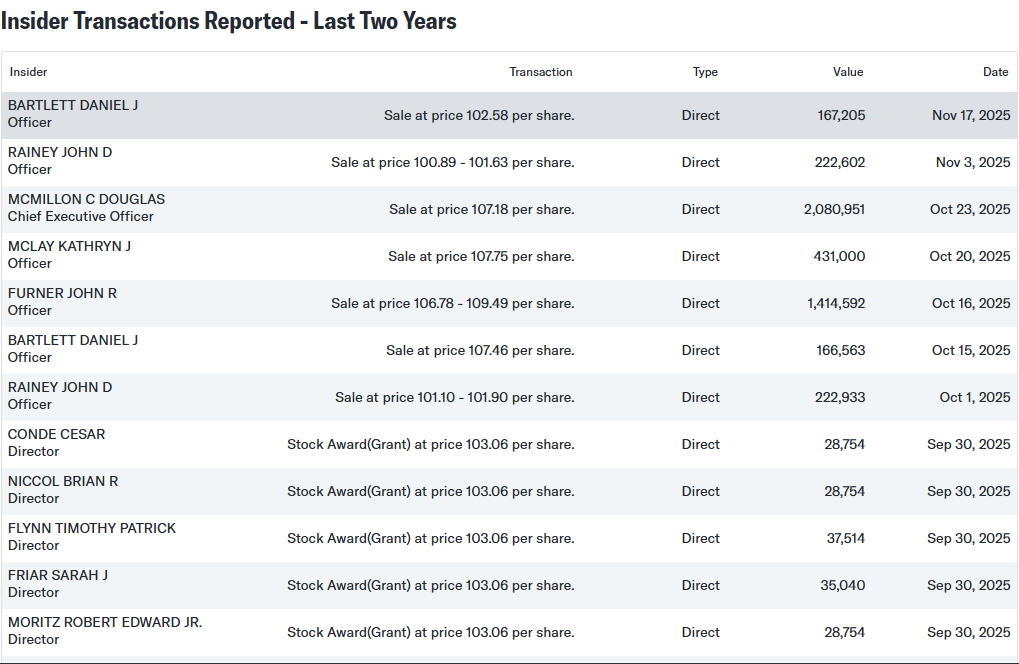

Insider Trading

Illustration 25: Most recent insider trading at Walmart, gathered from Walmart Inc. (WMT) Recent Insider Transactions – Yahoo Finance. Please consult yahoo finance for most updated list.

In recent months, Walmart insiders have sold a significant amount of stock, which can be considered a red flag for investors. The Walton Family Holdings Trust, which owns roughly 10% of the company, sold 7.56 million Walmart shares worth about $740.9 million. CEO Doug McMillon also sold 19,416 shares at prices between $95.97 and $96.09 and Executive Vice President John R. Furner sold 13,125 shares at prices ranging from $106.38 to $109.51. Most of these sales were conducted under prearranged Rule 10b5‑1 trading plans. These plans allow insiders to sell shares according to a pre-approved schedule. The scale of these transactions is notable. This could signal that insiders believe the stock is overvalued.

Rule 10b5‑1 plans reduce the likelihood that trades reflect a sudden loss of confidence. Despite this, the combination of large insider sales and Walmart’s high valuation suggests caution. It may indicate that key executives and major shareholders are taking profits while the stock price is elevated, which can be a warning sign for potential investors. Walmart’s insider trading policy requires trades to occur during open windows. They must also be under pre-approved plans. This provides governance oversight. However, the recent activity still highlights that insiders are reducing their exposure.

Overall, the scale and timing of these insider sales is a red flag, suggesting that Walmart may be trading at a premium and long-term investors should consider this carefully when evaluating the stock.

Other Company Info

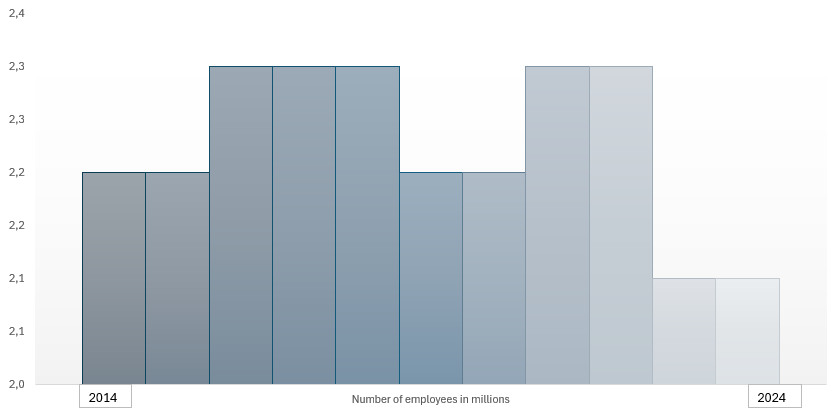

Founded in 1962, Walmart Inc. is one of the world’s largest and most recognized retail corporations, known for its extensive store network, low prices and growing e-commerce operations. As of 2024, Walmart employs approximately 2.1 million people globally, reflecting its vast operations in retail, supply chain, logistics and digital commerce. The company is publicly traded on the New York Stock Exchange under the ticker symbol WMT and operates within the Consumer Staples sector, specifically in the Retail—Discount Stores industry.

Walmart is headquartered at 702 S.W. 8th Street, Bentonville, Arkansas, USA. As of 2024, the company has approximately 2.82 billion shares outstanding, with a market capitalization of over $470 billion USD. For more information, visit Walmart’s official website: https://corporate.walmart.com

Illustration 26-28: Number of employees and location of Walmart

Final Verdict

Overall, Walmart is not recommended as a value investment at this time. The stock appears significantly overpriced, with a high P/E ratio, elevated insider selling, and a price well above historical levels. While Walmart remains a financially strong company with solid operations, steady dividends, and improving profitability in recent years, the current valuation limits upside potential for long-term investors. Retail as a sector is also highly competitive

Your message has been sent

Leave a Reply