Introduction – Born with Nothing but Fire in his belly

It all began in 1956 in the heart of horse country, Lexington, Kentucky. Picture a small home, chipped paint, a cracked driveway, and a fridge that was more often empty than full. This was the world John Bryan Morgan was born into. His childhood wasn’t bathed in luxury. No designer clothes, no trust funds, no summer getaways to Europe. What he had instead was a relentless fire in his belly, a hunger for something bigger.

Illustration1: John Morgan, the legend behind it all.

John was one of five siblings in a working-class family that often struggled to make ends meet. His father, a meat cutter with a troubled relationship with alcohol, would sometimes disappear into his vices, leaving his wife, John’s mother, to keep the family afloat. She was the real-life Wonder Woman. No cape. No superpowers. Just grit and an unbreakable sense of duty.

Even as a child, John knew life wasn’t fair. Other kids had allowances. He had chores. While others played video games, he was mowing lawns, washing dishes and hustling in every way he could.

And yet, even amid poverty, there was something special about young John. He was observant, sharp and most importantly, he had a dream. He wasn’t sure what it was yet, but he knew it didn’t involve staying poor.

Illustration 2: Kentucky, the humble start of John Morgan

College Dreams and Detours

John was determined to break the cycle. He knew education was the key, the great equalizer. He managed to claw his way into the University of Florida, a major leap for a kid from the working-class South. But college wasn’t a picnic. It was a battlefield.

To afford tuition, John worked a series of odd jobs, from dishwashing to nighttime security. He studied by the dim glow of streetlamps. He skipped meals. He bought used textbooks with notes scribbled all over them. But he never complained. Not once. Because he was building his future, one late-night cram session at a time.

After undergrad, John set his sights on law school. He got into the University of Florida Levin College of Law, where he was surrounded by peers from elite families, meaning kids who rolled up in BMWs while he was still patching holes in his shoes. But he didn’t care. He wasn’t there to impress, he was there to dominate.

He graduated in 1983, not just with a degree, but with a vision. He didn’t want to work for the rich. He wanted to fight for the people who had no voice, people like his mom, like his friends back in Kentucky, like himself.

Illustration 3: Morgan didn’t let the fact that he wasn’t rich or his social status bring him down.

The Birth of a Giant: Morgan & Morgan

In 1988, John Morgan did something insane, he left the comfort of an established firm and started his own with barely a handful of clients and next to no money.

He and his wife Ultima, a fellow lawyer, worked from a tiny office in Orlando, scraping together clients and praying they could make rent. There was no glitz, no glam, no waiting list of millionaire clients. It was just John, Ultima, a desk, a phone and a dream. But John had something most lawyers didn’t, the courage to advertise.

Back then, legal advertising was frowned upon. It was seen as “low-brow” even tacky. But John saw the future. He started running commercials, putting up billboards and buying ad spots on radio and TV. It was revolutionary. His face became instantly recognizable. His firm’s phone began to ring off the hook. And slowly but surely, Morgan & Morgan became a name people trusted.

Traditional firms sneered. Some even mocked him openly. But guess what? It worked. The phone lines lit up. Working-class Americans, immigrants, single mothers, veterans and everyday folks finally saw a lawyer who seemed to get them, a lawyer who didn’t look down on them, but stood beside them.

John knew that justice shouldn’t be reserved for the rich. He created a firm that operated on contingency meaning clients paid nothing unless the firm won. This flipped the power dynamic of law on its head. Suddenly, people who could never afford an attorney were getting high-powered representation. And they were winning.

Illustration 4: John Morgan’s formula of success lies in his use of advertisement.

Word spread. Morgan & Morgan began adding attorneys. Then offices. Then entire teams dedicated to intake, investigations, case management and trial. The small Orlando firm morphed into a regional force, then a national powerhouse.

But the firm wasn’t just growing, it was innovating. John implemented cutting-edge call centers and custom legal software to manage thousands of cases simultaneously. He invested in digital ads and SEO when other firms were barely online. He brought in experts in analytics, data and marketing to scale the business like a Silicon Valley startup.

By the 2000s, Morgan & Morgan had become a juggernaut. John kept his foot on the gas, opening offices in nearly every major city. The firm handled cases involving everything from medical malpractice and product liability to class actions and even civil rights.

Today, Morgan & Morgan has over 800 attorneys and 3,000 staff members. It serves clients in all 50 states and handles more than half a million cases each year. It’s not just the largest injury law firm in America, it’s one of the most recognized legal brands in the world.

Illustration 5: Morgan & Morgan has now more than 800 attorneys and run ads nationwide not only in Orlando where it all started.

John Morgan didn’t just start a law firm. He built a legal empire with a mission so clear it’s tattooed on the American psyche: “For The People.”

And that empire? It all started in a tiny Orlando office, with a man who believed that no one should have to fight alone.

From the Courtroom to the Boardroom

John Morgan didn’t just want to win cases, he wanted to bend the entire legal universe to his will.

Picture this: most lawyers were grinding away on measly slip-and-fall cases, chasing billable hours like hamsters on a wheel. John? He was building an empire. While the rest of the legal world was stuck in the 1980s, he was already thinking like Jeff Bezos with a briefcase.

He turned his firm into a litigation factory, but not in a sleazy ambulance-chaser way this was industrial-strength lawyering. Car accidents? Handled. Medical malpractice? Crushed. Class-action lawsuits? Bring it on. If David had a case against Goliath, Morgan & Morgan would’ve filed it before sunrise.

He pioneered a flat-fee structure, built a literal in-house call center to handle thousands of daily inquiries, and invested in tech like he was the Mark Zuckerberg of lawsuits. Imagine Apple HQ, but instead of iPhones, they were cranking out million-dollar verdicts.

Soon, he was on the talk-show circuit, dishing out unfiltered wisdom. He wrote books that didn’t just sit on dusty law school shelves, they hit bestseller lists.

His book “You Can’t Teach Hungry” was part pep talk, part street-fight manual, and part “Morgan gospel.” The thesis was simple: hustle like hell, be unapologetically yourself and never forget who you’re fighting for.

The Man behind the money

Now, you’d think a billionaire lawyer would be a stiff in a tailored Armani suit, sipping a $500 Scotch in some mahogany-lined office. Not John.

Illustration 6: Morgan was never stiff or elitist like other lawter, but he was relatable and liked the same things as an average american like a good Cuban sandwitch.

The man loves fried chicken. He loves Cuban sandwiches so much he’s practically a sandwich influencer. He puffs cigars like he’s starring in his own gangster flick, and he tweets jokes that make you wonder if your lawyer is secretly running a comedy club on the side.

He’s approachable, funny, and dare I say it dangerously relatable. And that’s why people adore him.

But peel back the jokes, and you find someone who cares deeply. Morgan has donated millions to causes like education, poverty relief, and criminal justice reform. One of his fiercest crusades? Medical marijuana.

This wasn’t about trend-chasing or headlines. This was personal. His brother, Tim, suffered from a devastating spinal cord injury, and medical marijuana was the only thing that gave him relief. John didn’t just sympathize, he fought. He poured millions into Florida’s 2016 Amendment 2 campaign and helped legalize medical marijuana statewide.

Not because it was fashionable. Not because it was profitable. But because it was right. Because family came first

The Billionaire Nobody Saw Coming

John Morgan didn’t wake up one day and say, “I want to be a billionaire.” He just kept building, winning, investing and suddenly, there it was.

Hotels? He bought them. Real estate? He stacked it like Monopoly pieces. Cannabis startups? Yep, he planted those seeds too. By the time anyone noticed, John had quietly become the billionaire nobody expected.

Sure, he’s got the toys: a mansion in Lake Mary, Florida, that looks like something out of MTV Cribs.

A fleet of cars. A private jet. A yacht. Probably a secret lair under the mansion for good measure.

But here’s the kicker: he’s still the same fried-chicken-loving, Cuban-sandwich-tweeting, people’s lawyer he always was. If you ask him about his proudest achievement, he won’t say “the billions.” He’ll say it’s his employees who love him, the thousands of clients whose lives he helped rebuild, and the fact that when people hear the name “Morgan,” they think trust.

Illustration 7: Morgan didn’t let his money change who he was.

The Media Mogul and the Meme Machine

Advertising? John Morgan doesn’t just do it, he dominates it. His law firm commercials are the stuff of legend. Funny, bold, slightly absurd and absolutely unforgettable.

And then there’s social media. Most billionaires hire a PR team to write robotic posts. John Morgan? He’s tweeting his own jokes, ranting about insurance companies, and casually dropping lines about running for president. One day he’s a lawyer. The next? A meme.

But here’s the genius: he leaned into it. He became the meme. He is the meme. He understood what most tycoons don’t: in the modern world, authenticity beats polish. Every time.

Illustration 8: John Morgan used memes, tweets and advertising heavly to his advantage.

For the People

Everything John Morgan built, everything, comes back to one mantra: For The People.

It’s not just a slogan slapped on a billboard. It’s the heartbeat of his firm. Today, Morgan & Morgan handles over 500,000 cases a year, a mind-boggling number that makes them less of a law firm and more of a justice delivery system.

He mentors young lawyers, invests in progressive causes and keeps pushing the boundaries of what a law firm can do. His sons are stepping into the game, learning the ropes, gearing up to take the Morgan legacy even further.

And John? He’s not even close to done. He might run for office. He might launch a bourbon brand called “For the Pour.” He might buy a baseball team just for the fun of it. Whatever it is, you can bet it’ll be big, bold, hilarious and very, very John Morgan.

Final Thoughts: The Legend of John Morgan

From the dirt roads of Kentucky to billion-dollar boardrooms, John Morgan’s story is the ultimate “American dream with a punchline.”

He didn’t just beat the odds, he rewrote them. He showed us that grit, guts and a sense of humor can take you from nothing to an empire.

He started with nothing. He gave everything. And he built a kingdom, for the people.

And if you don’t believe me, just wait because the next chapter of John Morgan’s story is probably going to be wilder than the last.

Illustration 9: John Morgan knew the power of humor and advertising.

India is more than just a country, it is a civilization that spans thousands of years, a vibrant continent in its own right, and an economic marvel constantly in motion. With a history that stretches back over five millennia, India remains one of the world’s oldest cultures while simultaneously being one of the youngest and fastest-growing economies on the planet.

Today, it stands as the most populous nation on Earth, the fifth-largest economy by nominal GDP, and a powerhouse of innovation and entrepreneurship. The economy of India is a developing mixed economy with a notable public sector in strategic sectors.

Known as the world’s largest democracy, India is a federal republic composed of 28 states and 8 union territories. It is a nuclear-armed nation, a member of influential groups such as the G20, BRICS, and the World Trade Organization, and holds a pivotal position in the Indo-Pacific region both strategically and economically.

As of 2024, India’s nominal GDP reached nearly $3.9 trillion, edging past the United Kingdom and approaching the size of Germany’s economy. When measured in purchasing power parity terms, India ranks third globally behind China and the United States. This remarkable economic ascent is fueled by a young and expanding population of 1.44 billion people, a rapidly growing middle class, and a labor force increasingly skilled in technology and services.

his article explores the complex and fascinating story of India’s economic evolution, from its early days of immense wealth through the hardships of colonialism, the challenges of socialist policies, and finally the remarkable liberalization that catapulted the nation into the global spotlight. Whether you are an investor, student, or simply curious about global affairs, India’s economic journey offers profound lessons in resilience, ambition, and transformation.

Historical Background

India’s history as an economic power dates back thousands of years, when it accounted for roughly a quarter to a third of the world’s GDP. During ancient times, great empires such as the Mauryas, Guptas, Cholas, and later the Mughals presided over prosperous kingdoms that exported textiles, spices, gems, and rich cultural knowledge to distant lands. India’s early economy was sophisticated and globally connected, making it one of the wealthiest regions on Earth.

India’s history as an economic power dates back thousands of years, when it accounted for roughly a quarter to a third of the world’s GDP. During ancient times, great empires such as the Mauryas, Guptas, Cholas, and later the Mughals presided over prosperous kingdoms that exported textiles, spices, gems, and rich cultural knowledge to distant lands. India’s early economy was sophisticated and globally connected, making it one of the wealthiest regions on Earth.

Illustration 2: Mughal Empire of India

However, the arrival of European colonial powers, especially the British East India Company in the 18th century, marked a profound shift. What was once a manufacturing and trading powerhouse became a supplier of raw materials and a captive market for British goods.

The colonial period saw the systematic deindustrialization of India’s traditional industries, such as the famous textile mills of Bengal, and the extraction of wealth that hindered economic progress for nearly two centuries. By the time India gained independence in 1947, its share of the global economy had dwindled to a mere 3%, a shadow of its former glory.

Illustration 3: British India led to India falling from making up 22.6% of the world economy in 1700 to 3.8% in 1952.

After independence, India embarked on a path shaped by the vision of Prime Minister Jawaharlal Nehru, who championed a socialist-inspired model of economic development. The state took control of key industries such as heavy manufacturing, banking, railways, and energy.

While this helped establish a basic industrial base, it also resulted in the notorious “License Raj,” a cumbersome system of permits and bureaucratic controls that stifled entrepreneurship and economic dynamism. For decades, India’s growth rate lingered at a modest 3 to 4 percent, a pace so slow it was mockingly dubbed the “Hindu rate of growth.

The turning point came in 1991 when a severe balance of payments crisis forced India to fundamentally rethink its economic model. Led by Finance Minister Manmohan Singh, the government embarked on sweeping reforms that dismantled import restrictions, reduced subsidies, and opened the economy to foreign investment. This liberalization unleashed a wave of economic activity that transformed India into a global player. The IT sector boomed, telecom networks expanded, pharmaceutical companies grew to global prominence, and financial markets developed rapidly. India’s economy accelerated, foreign reserves surged, and the nation gained credibility on the world stage.

The Structure of the Indian Economy

India’s economy is broadly divided into three main sectors: agriculture, industry, and services. Together, these sectors weave a complex and sometimes contradictory tapestry. While agriculture still employs the largest share of the workforce, roughly 43% of the population, it accounts for only about 20% of GDP.

Illustration 4: The Indian economy is complex like a tapestry

Industry contributes around a quarter of the GDP and employs about a quarter of the labor force. The services sector dominates the economy, representing more than half of the country’s GDP, yet employs only about a third of the workers. This structural imbalance highlights some of India’s greatest development challenges but also points to immense opportunities for growth and modernization.’

1. Industry and Manufacturing

Historically a late bloomer in manufacturing, India has increasingly turned its attention to industrial development. The government’s flagship initiative, “Make in India,” aims to expand the manufacturing sector’s share of GDP to 25 percent.

he automobile sector is one of the largest in the world, with companies like Tata Motors, Mahindra & Mahindra, bajaj auto, TVS motor company, Atul Auto and Maruti Suzuki producing millions of vehicles annually. As of 2023, India ranked as the fourth-largest automobile producer in the world, following China, United States and Japan. T

he sector accounts for approximately 7.1% of India’s GDP and employs over 37 million people directly and indirectly. As of April 2022, India’s auto industry is worth more than US$100 billion and accounts for 8% of the country’s total exports and 7.1% of India’s GDP.

Illustration 5: India is one of the world’s largest producers of tuk tuks

The pharmaceutical industry, often called the “pharmacy of the world,” manufactures 60 percent of the world’s vaccines and is a global leader in generic drugs. Heavy industries such as steel, cement, and chemicals are dominated by conglomerates like Tata Steel and Aditya Birla Group.

India is also carving a niche in emerging industries such as semiconductors, solar energy equipment, and electric vehicles, with states like Gujarat and Tamil Nadu competing fiercely to attract large factories and investment. Defense manufacturing is another growing priority, as India seeks to reduce its dependence on arms imports and develop indigenous capabilities.

Mining contributed to 1.75% of GDP and employed directly or indirectly 11 million people in 2021. India’s mining industry was the fourth-largest producer of minerals in the world by volume, and eighth-largest producer by value in 2009.

In output-value basis, India was one of the five largest producers of mica, chromite, coal, lignite, iron ore, bauxite, barite, zinc and manganese; while being one of the ten largest global producers of many other minerals.

Illustration 6: Rajesthan is one of the indian states with the most natural resources

Indian cement industry is the 2nd largest cement producing country in the world, next only to China. At present, the Installed Capacity of Cement in India is 500 MTPA with production of 298 million tonnes per annum. Majority of the cement plants installed capacity (about 35%) is located in the states of south India.

India surpassed Japan as the second largest steel producer in January 2019.The country’s steel sector benefits from abundant iron ore reserves, a large labor force, and strong government support through initiatives like “Make in India” and the National Steel Policy. As demand for steel rises both domestically and globally, India continues to expand its production capacity and export footprint.

Petroleum products and chemicals are a major contributor to India’s industrial GDP, and together they contribute over 34% of its export earnings. India hosts many oil refinery and petrochemical operations developed with help of Soviet technology such as Barauni Refinery and Gujarat Refinery, it also includes the world’s largest refinery complex in Jamnagar that processes 1.24 million barrels of crude per day.

By volume, the Indian chemical industry was the third-largest producer in Asia, and contributed 5% of the country’s GDP. India is one of the five-largest producers of agrochemicals, polymers and plastics, dyes and various organic and inorganic chemicals. Despite being a large producer and exporter, India is a net importer of chemicals due to domestic demands. India’s chemical industry is extremely diversified and estimated at $178 billion.

India is one of the largest producers and consumers of chemicals and fertilizers in the world, with the chemical industry contributing over 7% to the country’s GDP and ranking 6th globally in chemical production. At present, 57 large fertilizer units are manufacturing a wide number of nitrogen fertilizers. These include 29 urea-producing units and 9 ammonia sulfate-producing units as a by-product. Besides, there are 64 small-scale producing units of single super phosphate.

The fertilizer sector, vital for India’s agriculture, produced around 43.7 million tonnes of fertilizers in 2024–25, including urea, DAP, and complex fertilizers, supported by government subsidies and increasing adoption of nutrient-based fertilizers. The growing demand from agriculture, textiles, and pharmaceuticals continues to drive expansion in both sectors.

Illustration 7: India is one of the largest producers of dye in the world.

Furthermore, when it comes to transportation India is the third-largest domestic aviation market in the world, with passenger traffic reaching over 280 million in 2023. As of 2024, the country has 149 operational airports, up from 74 in 2014, and the government plans to expand this to 220 airports by 2030 under a 1 trillion Indian rupees infrastructure push.

India’s railways, contributing about 2% to the country’s GDP, transport over 8 billion passengers and 1.2 billion tonnes of freight annually, making it one of the world’s largest and busiest rail networks. The sector supports around 7 million jobs, both directly and indirectly, playing a crucial role in driving economic growth and connecting markets across the nation. With ongoing investments in modernization, electrification, and high-speed rail, Indian Railways is set to boost productivity and sustainability even further.

Illustration 8: Mumbai train station

India also has multiple ship building companies such as Cochin Shipyard, Hindustan Shipyard and Swan Defence and Heavy Industries, mainly produces ships for European, South American and African shipping companies. Cochin shipyard is the pioneer in autonomous electric propulsion ships.

2. Agriculture – The Paradox of Inida’s economy

Agriculture remains the cornerstone of India’s socio-economic landscape, deeply intertwined with the lives of over 40% of the population who depend on it for their livelihoods. Despite its declining share of around 16-17% in the country’s GDP, the sector is critical for ensuring food security, sustaining rural communities, and maintaining social stability across vast regions.

India proudly holds the title as the world’s largest producer of milk, pulses, and spices, and is among the top global producers of staples like rice, wheat, sugarcane, cotton, and a wide variety of fruits and vegetables, feeding over 1.4 billion people.

Yet, beneath this agricultural abundance lies a paradox: low productivity and fragmented landholdings often limit farmers’ incomes and economic resilience. Most farms are small, averaging less than 2 hectares, which constrains the adoption of advanced technology and efficient farming practices.

Additionally, frequent climate shocks, such as droughts, floods, and erratic monsoons, leave millions vulnerable and threaten crop yields year after year. Infrastructure challenges, including inadequate irrigation, poor storage facilities, and inefficient supply chains, further reduce farmers’ ability to maximize profits and reach larger markets.

Illustration 9: India is one of the largest producers of tea

Recognizing these challenges, India has embarked on a path to modernize agriculture by investing in better irrigation systems, promoting mechanization, improving rural roads and cold storage, and embracing digital technologies like satellite imaging and mobile apps to provide real-time information to farmers.

India’s agriculture and allied sectors remain a vital part of the economy, accounting for 18.4% of GDP and employing nearly 46% of the workforce, despite the sector’s shrinking share in overall economic output, from 52% in 1951 to around 15% in 2023.

The country boasts the largest arable land area in the world, ranking as a top global producer of milk, pulses, spices, rice, wheat, sugarcane, cotton, fruits, and vegetables. However, productivity challenges persist, with yields often only 30% to 50% of global best practices due to small landholdings, inadequate irrigation (only about 39% of cultivated land is irrigated), and infrastructure gaps in storage, roads, and markets. These issues limit farmers’ incomes and keep agricultural output below its full potential.

India is also a global leader in fisheries and aquaculture, ranking 3rd and 2nd respectively, providing livelihoods to millions, and exporting significant quantities of processed products like cashew kernels and milk. While the country produces roughly 316 million tonnes of foodgrains annually, stagnation in output and large post-harvest losses, up to one-third of production, highlight inefficiencies.

Government initiatives like the ₹1.2 trillion Accelerated Irrigation Benefit Programme aim to improve irrigation and infrastructure, but regulatory hurdles and market constraints continue to slow progress. Overall, India’s agriculture sector is a complex blend of immense scale, rich diversity, and urgent need for modernization to boost productivity and farmer prosperity.

Illustration 10: Indian women pounding rice, India is one of the world’s largest rice producers

However, progress has been uneven and often slowed by political sensitivities and social complexities. The massive farmer protests of 2020–21 underscored the deep-rooted concerns and emotional ties surrounding land rights, pricing, and market reforms. These protests highlighted how any attempt to transform India’s agricultural sector must carefully balance economic modernization with the protection of farmers’ livelihoods and rights.

Looking ahead, the future of Indian agriculture depends on successfully navigating this delicate balance, integrating technology and innovation while ensuring inclusivity and sustainability. With targeted reforms, climate-resilient farming practices, and strengthened rural infrastructure, India has the potential not only to feed its vast population but also to emerge as a global leader in sustainable agriculture.

3. Services – The Crown Jewel

The services sector has emerged as the undisputed engine of India’s economic growth, contributing a staggering over 50% of the country’s GDP, making it the largest sector in the Indian economy. From IT and software exports to financial services, healthcare, education, telecommunications, tourism, logistics, and more. the breadth and dynamism of this sector reflect India’s transition from a primarily agrarian economy to a global services leader.

Illustration 11: The city of Hyderabad is becoming a global hub for IT.

Cities like Bengaluru, Hyderabad, Gurugram, and Pune have become world-renowned hubs for IT, software development, business process outsourcing (BPO), and innovation, attracting investments from global tech giants and startups alike.

India’s Information Technology and Business Process Management (IT-BPM) sector alone generated over $250 billion in revenue in 2023, employing more than 5 million professionals, and contributing significantly to foreign exchange earnings.

Indian IT firms serve clients across the globe, from Silicon Valley startups to Fortune 500 corporations, delivering everything from cloud computing to AI solutions. Beyond tech, India’s financial services sector, anchored by robust public and private banks, insurance companies, fintech startups, and stock exchanges like NSE and BSE, plays a pivotal role in capital formation and investor confidence.

India’s telecom sector is a global giant, now the second-largest market in the world with over 1 billion phone subscribers and one of the lowest call tariffs due to intense competition. In FY 2024, telecom equipment production crossed ₹45,000 crore, with exports hitting ₹10,500 crore, driven by the booming smartphone manufacturing industry. India also ranks among the top three globally in internet users, and is the largest DTH television market by subscribers making digital connectivity a key pillar of its economic growth.

Equally significant is the rise of tourism, healthcare, education, retail, e-commerce, and digital services, all of which are rapidly expanding with the growing urban middle class and increasing internet penetration. The Unified Payments Interface (UPI) revolutionized digital transactions, processing billions of transactions monthly, and helped formalize vast segments of the economy. Meanwhile, the services sector has also become a major employment generator, especially in urban and semi-urban areas, offering opportunities in both high-skilled and low-skilled segments.

The government’s focus on initiatives like Digital India, Skill India, and Start-Up India further accelerates the services sector’s potential, promoting entrepreneurship, digital infrastructure, and employment. However, to sustain this momentum, India must address key challenges, such as improving ease of doing business, upskilling the workforce, enhancing service exports, and bridging the digital divide in rural areas.

In essence, the services sector is not just a component of India’s economy, it is its beating heart, transforming the country into a knowledge-based, innovation-driven powerhouse that is well on its way to becoming a major player in the global economic landscape.

Innovation and the Digital Revolution

India’s 63 million MSMEs (Micro, Small, and Medium Enterprises) contribute 35% to GDP, employ over 111 million people, and make up 40% of exports, earning their title as the “growth engines” of the economy. Though 90% are micro-enterprises with limited scale, 2023 saw a record 179 SME IPOs, showing rising investor interest. With continued policy support and reforms, MSMEs hold the key to tackling unemployment and driving inclusive growth.

India’s digital transformation has been nothing short of revolutionary. Central to this has been the Unified Payments Interface (UPI), a real-time digital payment system that processes billions of transactions monthly, outpacing even the combined digital payments of the US, China, and the EU. The Aadhaar biometric identification system has provided over 1.3 billion Indians with a unique digital identity, enabling unprecedented access to banking, government services, and welfare programs.

Together with the Jan Dhan-Aadhaar-Mobile (JAM) trinity, these innovations have democratized access to finance and services across vast rural and urban populations. The government’s Digital India initiative aims to further embed technology into governance, business, and daily life, while targeted programs such as Startup India and the Semiconductor Mission are propelling innovation and domestic manufacturing.

Furthermore, India’s youthful population is one of its greatest assets. With a median age of just 28.4 years, India is far younger than many developed countries whose median ages often exceed 40. Each year, approximately twelve million young people enter the labor market, creating both an opportunity and a challenge to generate sufficient employment. By 2030, India is expected to be home to seven megacities and more than 600 million urban residents, fueling demand for housing, infrastructure, transportation, and services.

Illustration 12: India’s population is very young something that can become its great asset.

The key to harnessing this demographic dividend lies in education and skills training to ensure that young Indians are productive contributors to the economy rather than unemployed or underemployed.

India’s cultural richness and heritage form a vital pillar of its economy. The country attracted more than 17 million tourists in 2023, contributing significantly to local economies.

Beyond the traditional pilgrimage and heritage tourism sectors, India’s global influence is bolstered by Bollywood, yoga, cuisine, cricket, and festivals that resonate worldwide. The Indian diaspora, numbering over 30 million people globally, acts as a powerful cultural and economic bridge, enhancing India’s soft power and international reputation.

Illustration 13: A Bollywood poster

Trade and Global Integration

India’s role in global trade continues to expand rapidly. As the world’s ninth-largest exporter of goods and sixth-largest importer, India’s export basket includes refined petroleum, gems and jewelry, pharmaceuticals, automobiles and parts, and software services. The United States, China, the United Arab Emirates, the European Union, and ASEAN nations are India’s most significant trading partners.

India is actively negotiating free trade agreements with major economies like the UK and the EU and is building regional supply chains to reduce reliance on China and enhance economic resilience. On the global stage, India positions itself as a leading voice for the developing world, championing issues such as debt relief, food security, and climate action, especially during its G20 presidency in 2

Credit Score

India currently holds a sovereign credit rating of “BBB-” with a stable outlook from S&P and Fitch, and a “Baa3” from Moody’s, both of which are the lowest investment-grade ratings. These ratings indicate that India is a relatively safe destination for investment, but with moderate credit risk. The scores reflect a balance between India’s strong long-term growth prospects and structural economic challenges such as a high fiscal deficit, significant public debt, and dependency on imported energy.

The rating agencies acknowledge India’s resilient and diversified economy, large domestic market, improving infrastructure, and digital innovation as strengths. India’s track record of stable democratic governance, reforms in taxation (like GST), and emphasis on infrastructure and ease of doing business further support its rating. However, concerns remain over fiscal discipline, with the government debt-to-GDP ratio hovering around 83%, and recurring fiscal deficits above 5%, driven by subsidies, welfare schemes, and lower tax revenues.

Despite global economic uncertainties, India’s strong GDP growth, estimated at around 6–7% annually, even during volatile periods, continues to reinforce investor confidence. Many experts believe that with continued reforms, improved tax collection, and responsible fiscal management, India could see a credit upgrade in the coming years, which would lower borrowing costs and attract more foreign investment.

Challenges and contradictions

Despite its impressive rise, India faces deep-seated challenges. Income inequality is stark, with the richest one percent controlling more than 40% of the nation’s wealth. Structural issues such as unemployment. especially among youth and graduates, remain unresolved. While India has made strides in reducing corruption and improving ease of doing business, bureaucratic inertia and red tape still hinder many entrepreneurs.

Environmental problems loom large as well. Air pollution in cities frequently reaches hazardous levels, water scarcity threatens agriculture and urban centers, and climate change presents an existential risk to development gains. Public debt, while moderate compared to many developed nations, is rising and will require careful fiscal management.

Illustration 14: Ambani tower in India highlighting the difference between rich and poor in the country.

India’s Global Ambitions

Looking forward, India has set ambitious goals to become a $5 trillion economy by 2027 and to join the ranks of the world’s top three economic powers by 2050. The government’s vision of “Viksit Bharat,” or Developed India, aims for transformational progress by the centenary of independence in 2047.

Priority sectors include renewable energy, where India is already a global leader in solar power and has pledged to reach net-zero carbon emissions by 2070. Defense manufacturing, advanced technologies such as artificial intelligence and quantum computing, biotechnology, and infrastructure development are all central to India’s future growth plans.

Massive investments in freight corridors, expressways, and ports are underway to improve logistics and connect the vast country more efficiently.

Conclusion

India’s economy embodies a unique paradox. It is ancient and modern, fast-growing yet uneven, chaotic yet bursting with creative energy. Unlike the more streamlined and centralized economies of Germany or China, India’s democratic capitalism is messy and vibrant, shaped by millions of individual decisions, countless startups, and an energetic population.

Illustration 15: India is one of the fastest growing economies in the world.

Its rise is not just an economic story but a human one, about a nation harnessing its vast potential, striving to lift hundreds of millions out of poverty, and aiming to reshape the global economic order. As smartphones proliferate in small towns, solar panels spread across deserts, and coding campuses thrive in Bangalore and Hyderabad, India is writing a new chapter in the story of global growth.

India’s economy is a dynamic blend of traditional strength and modern innovation, driven by a powerful services sector, a vast and evolving agricultural base, and a rapidly growing industrial and manufacturing ecosystem. With a young population, expanding digital infrastructure, and consistent GDP growth averaging 6–7%, India is well-positioned to become one of the world’s leading economic powers. However, to fully unlock its potential, the country must address key challenges like unemployment, low agricultural productivity, infrastructure gaps, and fiscal discipline, while continuing to invest in reforms, technology, and human capital.

Let’s begin with a riddle that has baffled more than a few bright minds. Suppose I offer you a choice: either I hand you $1 million right now, or I give you a single penny today that doubles in value every day for 30 days. Which would you take?

Illustration 1: 100 USD, the highest USD note

Most people instinctively jump at the million-dollar offer. A million bucks in hand feels like a dream come true. That’s life-changing money, after all. But if you run the math on that humble penny, something astounding happens. On day five, it’s just 16 cents. On day ten, it’s still under $6. But by day twenty, it explodes past $5,000. And on day thirty? That penny is worth over ten million dollars.

That, in a nutshell, is the sheer power of compounding, the secret sauce behind many of the world’s wealthiest investors. And yet, it remains one of the most misunderstood, underestimated, and underused concepts in personal finance and trading alike. While others chase quick profits and high-risk trades, the smartest players in the game let time do the heavy lifting.

What Is Compound Investing, Really?

Compound investing is the financial equivalent of planting an apple tree and waiting patiently until you’re sitting in an orchard. At its heart, compounding means that your investments don’t just earn returns, they also earn returns on those returns. It’s a cycle of reinvestment, where growth builds upon growth, snowballing over time into something far greater than you started with.

Imagine putting $1,000 into an investment that earns 10% per year. After one year, you have $1,100. If you leave that full amount invested, the next 10% applies not just to your original $1,000, but to the $1,100 total which gives you $1,210. Then it grows to $1,331, then $1,464, and so on. Eventually, what started as a small seed becomes a forest of wealth.

Illustration 2: You don’t need to do anything, you can be on hammock in Indonesia and just relax if you want to

And the best part? You don’t have to do anything fancy. You don’t need a degree in finance or a crystal ball to time the market. You just need the discipline to start, the patience to wait, and the wisdom to let compounding do its thing.

Why Compound Investing Works Better Than Just About Anything Else

Let’s be blunt: most people want to get rich fast. We are hardwired to crave instant results. That’s why trading apps, meme stocks, and crypto roller coasters are so addictive. They feed the dopamine circuits in our brains. But in the long run, these fast strategies tend to burn more than they build.

Illustration 3: A lot of people such as those at the r/wallstreetbets subreddit focus on getting rich quick.

Compound investing, by contrast, doesn’t try to outsmart the market on a daily basis. It bets on consistency, not cleverness. Over long periods, compounding will often outperform flashy trading simply because it never stops working. Your capital keeps growing while you sleep, while you’re on vacation, while you’re living life. You don’t have to hustle, your money does it for you.

The real beauty of compound investing is that its effect accelerates over time. The longer you leave your investment untouched, the more explosive its growth becomes. This is why starting early is often more powerful than starting big.

The Mathematics of Miracles

The numbers behind compounding are not just impressive, they’re mind-blowing. Let’s take a simple scenario: you invest $10,000 at an 8% annual return, compounded once a year. In 30 years, that $10,000 becomes over $100,000. You didn’t lift a finger, yet your money grew tenfold.

Now, add a monthly contribution of just $300. That same investment explodes to nearly half a million dollars over the same timeframe. The math is straightforward, but the implications are profound. With time and consistency, even modest investments can turn into serious wealth.

Illustration 4: Over time compound interest can lead to serious wealth

There’s even a trick to estimate how long it takes for your investment to double: the Rule of 72. Just divide 72 by your annual return rate. At 8%, your money doubles in 9 years. That’s two doublings in 18 years, four in 36. It sneaks up on you, and suddenly, you’re looking at a portfolio that dwarfs what you ever imagined possible.

Compound Investing vs. Trading: The Showdown

Trading is sexy. It makes for great movies, exciting YouTube channels, and nail-biting nights staring at candlestick charts. But here’s the dirty little secret: most traders lose money. Not just some — most.

Illustration 5: Trading will eat up most of your capital that you could have used to become wealthy

The reasons are many. Transaction fees eat into profits. Emotions lead to poor decisions. Taxes hammer short-term gains. And worst of all, one bad trade can erase dozens of good ones. Trading rewards sharpness, but penalizes mistakes with brutal efficiency.

Compound investing plays a different game entirely. It’s slow, steady, and boring , in the best possible way. It rewards discipline, not luck. It minimizes fees, avoids taxes through long-term holding, and removes emotional triggers. While traders swing for the fences, compound investors jog steadily around the bases. And nine times out of ten, it’s the jogger who wins.

Illustration 6: An illustration showing the power of compound interest

Even in the trading world, the best players understand the power of compounding. They don’t gamble on every tick. They develop strategies that can grow capital sustainably. They think in terms of systems and longevity. In short, they let their skills and their capital compound over time.

Time: The Invisible Multiplier

If compounding is the vehicle, time is the fuel. Nothing supercharges compound investing like giving it time to work. And the earlier you start, the more time you have, the bigger your outcome.

There’s a famous story in finance circles about two hypothetical investors. One starts investing $200 a month at age 22 and stops at 30. The other waits until 30 and invests $200 monthly until retirement at 65. Guess who ends up with more money?

Illustration 7: Time is the fuel that powers it all

Surprisingly, the early starter wins, even though she contributed far less overall. That’s the power of compounding in action. The early years are the most valuable, because they multiply over the longest time. The longer your money compounds, the less you have to contribute later. The system does the heavy lifting.

What Happens If You Start Late?

Now, what if you’re reading this at 35, 40, or even 50 and feeling regret bubble up? Here’s the good news: it’s never too late to harness compounding. Yes, you’ll need to save more aggressively, and you may not have quite as much time. But compound investing still works.

Illustration 8: There is never to late to start compounding which is cause for celebtation

You can boost the effects by increasing contributions, reducing fees, reinvesting dividends, and choosing slightly higher-yielding (but still prudent) investments. The most important thing is to begin, not perfectly, but immediately.

Real Stories, Real Fortunes

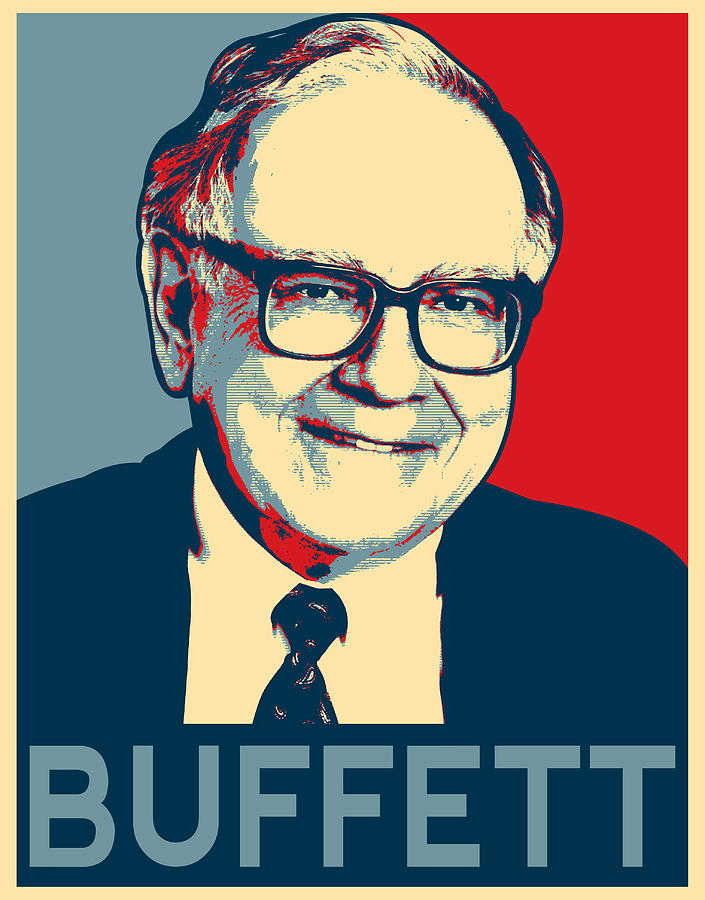

Warren Buffett, arguably the greatest investor of all time, built 99% of his wealth after the age of 50. He began investing at age 11 and never stopped. His wealth isn’t due to extraordinary returns, it’s due to extraordinary time. His investing returns have been great, sure — but it’s the decades of compounding that turned great into godlike.

Illustration 9; Legendary Investor Warren Buffet is someone that have built his wealth on compounding

Then there’s Ronald Read, a Vermont janitor who quietly amassed over $8 million through steady investing and compounding. Or Anne Scheiber, a retired IRS agent who left behind $22 million after years of investing modestly in dividend stocks. These weren’t hedge fund managers. They were regular people who simply understood compounding and never gave up on it.

The Investor’s Toolkit: How to Get Started

You don’t need a Wall Street advisor or a six-figure salary to begin. Open a brokerage account or a retirement fund. Automate monthly contributions, even if they’re small. Choose index funds or dividend-paying stocks with a history of stability and growth. Reinvest every dollar you earn. Then walk away. Let it grow.

Illustration 10: You don’t need to be a Wall Street investor to benefit from compound investing, a normal index fund like VOO or SPY will do.

The hardest part is resisting the temptation to tinker. When markets dip, and they will, don’t panic. Compounding doesn’t care about temporary downturns. It thrives over the long haul. The more hands-off you are, the better it works.

There are a few landmines that destroy compounding’s magic. The biggest is pulling out money too early. Every time you interrupt compounding, you reset the process. Another killer is chasing hot trends and high-risk stocks that can wipe out gains. High fees are another silent thief, quietly siphoning away your future wealth. And perhaps worst of all is waiting too long to start.

It’s easy to dismiss compound investing as “too slow” or “too dull.” But those who stick with it know the truth: it’s anything but boring. Watching your money grow, slowly at first, then exponentially, is one of the most thrilling experiences in finance. It feels like cheating — only it’s not.

Compound investing is the rare strategy that doesn’t just build wealth. It builds freedom. It buys you time, security, and peace of mind. It works when you sleep. It grows when you’re busy living. It’s not a sprint — it’s a quiet revolution, unfolding silently in the background.

Conclusion: Be the Turtle, Not the Rabbit

In the fable of the tortoise and the hare, it’s the slow, steady, unshakable turtle who wins the race. Compound investing is your turtle. It doesn’t promise instant riches. It doesn’t thrill with daily highs. But over time, it builds something far more valuable: lasting wealth.

Illustration 11: Be the turtle not the rabbit

In the fable of the tortoise and the hare, it’s the slow, steady, unshakable turtle who wins the race. Compound investing is your turtle. It doesn’t promise instant riches. It doesn’t thrill with daily highs. But over time, it builds something far more valuable: lasting wealth.

So stop chasing hot tips. Ignore the noise. Start investing, early if you can, consistently no matter what, and with patience above all. Let your money work harder than you ever could. Let compounding carry you toward the life you dream of.

Because once you understand compound investing, you’ll realize something extraordinary: you don’t have to get rich quick… when you can get rich for sure.

The Boeing Company is one of the world’s largest aerospace and defense corporations, renowned for its cutting-edge innovations in commercial aviation, space exploration, and military systems. Headquartered in Arlington, Virginia, Boeing plays a pivotal role in global mobility and national defense, supplying aircraft, satellites, and defense systems to customers across more than 150 countries.

Illustration1 : The Boeing logo, a global symbol of aviation excellence and aerospace innovation.

Boeing operates across several major sectors including commercial airplanes, defense, space, and security systems, as well as global services. It is best known for its iconic aircraft such as the 737, 777, and 787 Dreamliner, which have helped connect the world’s cities and economies. Beyond aviation, Boeing leads ambitious projects in space travel, advanced robotics, and autonomous flight technologies.

Unlike many traditional manufacturing companies, Boeing evolved from the pioneering age of aviation and has remained a dominant force throughout the 20th and 21st centuries. Its legacy of innovation, high-performance engineering, and large-scale systems integration makes it a cornerstone of the global aerospace and defense industry.

History

Boeing was founded in 1916 by aviation pioneer William E. Boeing in Seattle, Washington. Originally a small manufacturer of seaplanes, the company played a significant role in both World Wars, supplying military aircraft that proved decisive in combat. Post-World War II, Boeing helped usher in the Jet Age with the launch of the 707, the first successful commercial jetliner.

Illustration 2: Boeing 707, was the first successful commercial jetliner.

Boeing’s commercial success soared with aircraft like the 737, 747, and 777, revolutionizing long-distance air travel. The 747, in particular, became a global icon and the world’s first wide-body “jumbo jet,” transforming air travel in the 1970s.

In 1997, Boeing merged with McDonnell Douglas, strengthening its position in the defense sector. The company also expanded into space systems, becoming a key contractor for NASA, including work on the International Space Station, Space Launch System, and Starliner crew capsule.

Despite facing challenges such as the 737 MAX crisis, global supply chain issues, and geopolitical headwinds, Boeing continues to be a vital force in aerospace innovation and global defense capabilities.

Operations and Production

Portfolio

Boeing is one of the world’s leading aerospace companies, with core operations centered around the design, manufacture, and support of commercial airplanes, defense systems, satellites, and space exploration technologies.

Its flagship commercial aircraft include the 737, 747, 767, 777, and 787 Dreamliner families. With operations in over 65 countries and customers in more than 150, Boeing is one of the largest exporters in the United States.

Its operations are divided into three primary business units:

Illustration 3: A Boeing commercial plane landing.

Boeing Commercial Airplanes (BCA), which designs, assembles, and delivers aircraft to airlines and leasing companies. Boeing’s commercial aircraft families include 737 (The best-selling jetliner in history, primarily used for short- to medium-haul routes) and 787 Dreamliner (A long-haul, fuel-efficient wide-body aircraft made with composite materials).

Furthermore, it includes 777 and 777x ( Known for long-range and high-capacity, with the 777X featuring folding wingtips and the world’s most powerful jet engines), and 767 and 747-8 (used for both passenger and cargo operations, with the 747 being the iconic “Queen of the Skies).

Illustration 4: A Boeing Spy plane

The second division of Boeing is Boeing Defense, Space & Security (BDS) which delivers products and services to government customers worldwide. This includes: Combat aircraft such as the F/A-18 Super Hornet and F-15EX Eagle II. Furthermore it also includes Rotary-wing platforms like the AH-64 Apache and CH-47 Chinook helicopters.

Missile defense systems, satellites, and space launch systems including the Space Launch System (SLS), the most powerful rocket NASA has ever built, is also part of the BDS division of Boeing.

The third division is Boeing Global Services (BGS) which offers logistics, maintenance, training, parts, and digital aviation services. BGS supports both commercial and defense customers with end-to-end lifecycle services

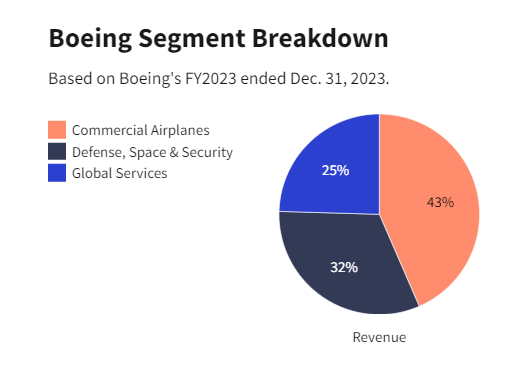

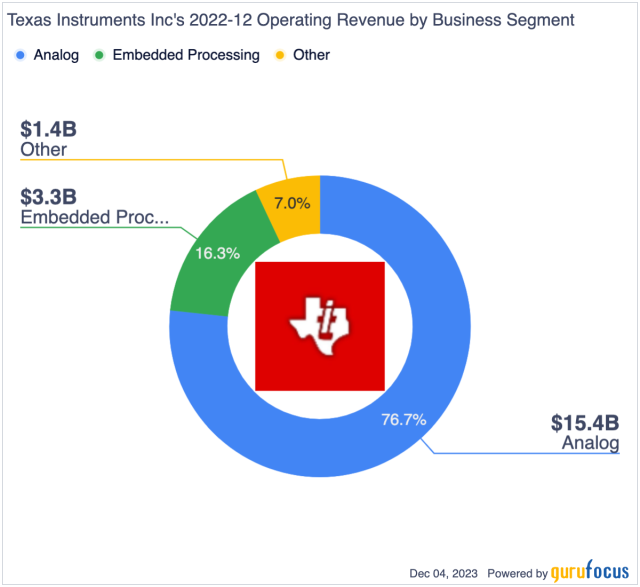

Illustration 5: Boeing revenue by segment

As can be seen from illustration 4, the largest segment for Boeing is commercial Airplanes at 43%. However, Defense, Space & Security also makes up a very big segment at 32% and Global Services at 25 %.

Boeing’s global manufacturing network includes major facilities in the U.S. (notably Everett and Renton, Washington; Charleston, South Carolina; and St. Louis, Missouri), along with significant operations in Australia, the U.K., Canada, and the Middle East.

Technology and Space

Boeing plays a key role in space exploration and defense innovation. Through its work with NASA, Boeing helped develop the International Space Station (ISS) and is now working on the Starliner spacecraft, designed to transport astronauts to low Earth orbit.

In defense, Boeing is investing in autonomous systems such as the MQ-25 Stingray (an unmanned aerial refueling aircraft), loyal wingman drones, and space-based missile defense technologies. Boeing is also a key player in hypersonic weapons development and satellite constellations for secure communications and Earth observation

In the AI and digital space, Boeing uses advanced analytics, machine learning, and digital twins to optimize manufacturing, maintenance, and flight operations. he company’s “AnalytX” suite supports real-time fleet health monitoring, and its digital solutions are integrated into flight operations globally.

Illustration 6: Loyal Wingman, an AI-enabled drone developed in Australia, designed to operate alongside manned fighter jets.

Key Competitors

Boeing competes across various aerospace and defense sectors. Its competitors differ depending on whether the focus is on commercial aviation, defense contracts, or space exploration.

1. Commercial Aviation

Airbus SE is Boeing’s primary global competitor in commercial aircraft. Airbus’s A220, A320neo, and A350 families compete head-to-head with Boeing’s 737 MAX, 787, and 777 series.

COMAC is backed by the Chinese government, COMAC aims to reduce reliance on Western aircraft through its C919 and ARJ21 models.

Embraer is a leading manufacturer of regional jets, Embraer was once part of a failed merger with Boeing but remains a strong player in the 70–150 seat market.

2. Defense and Military Systems

Lockheed Martin, dominates in fighter aircraft and space systems with platforms like the F-35 and Orion.

Northrop Grumman is a competitor in autonomous aircraft, strategic bombers (B-21 Raider), and satellite systems.

Raytheon Technologies, provides engines (via Pratt & Whitney), avionics, and missile systems used in both commercial and military platforms.

3. Space and Emerging Tecg

SpaceX, Elon Musk’s company is a disruptive force in spaceflight, reusable rockets, and low Earth orbit (LEO) satellite networks (Starlink).

Blue Origin is competing with Boeing for lunar landers and suborbital space tourism.

Palantir, Anduril is tech firms, entering defense with AI-powered battlefield intelligence and surveillance systems.

Competitive Advantage

Boeing’s competitive advantage is rooted in its scale, technical expertise, and diverse operations across commercial aviation, defense, and space.

As one of the oldest and most recognized names in aerospace, Boeing benefits from a strong brand reputation built on decades of delivering reliable, high-performance aircraft and systems. This reputation fosters long-term trust and loyalty among airlines, governments, and space agencies worldwide.

Illustration 7: A Boeing Aircraft flying over the Alps

The company’s vertically integrated operations and vast global supply chain give it the ability to manufacture complex systems at scale, while also adapting to local markets and geopolitical shifts. Boeing’s Global Services division adds further value by offering lifecycle support, digital solutions, and predictive maintenance, deepening customer relationships beyond the point of sale.

Boeing’s broad product portfolio, from narrow-body jets and wide-body aircraft to fighter jets, satellites, and launch vehicles, allows it to spread risk and capture opportunities in multiple markets. During commercial downturns, its defense and space segments provide financial stability and continuity.

Innovation is another core strength. Boeing continuously invests in advanced manufacturing, autonomous systems, artificial intelligence, and sustainable technologies. Programs like the ecoDemonstrator test platform and partnerships in urban air mobility demonstrate its commitment to shaping the future of flight.

Illustration 8: A Boeing 777

Combined with its global presence and government partnerships, Boeing’s ability to integrate technology, scale, and service gives it a clear edge in a highly competitive industry.

Future Outlook

Boeing is entering a new growth phase as the aviation industry rebounds and global demand for commercial aircraft returns. The company is ramping up production of its 737 MAX and 787 models, while its defense and space divisions continue to secure major contracts, especially in the U.S. and Asia-Pacific.

Sustainability is at the core of Boeing’s future strategy, with investments in sustainable aviation fuels, electric and hydrogen propulsion, and next-generation aircraft. Its space ventures, including the Starliner and Space Launch System, position Boeing to play a major role in future space exploration. With a strong order backlog and focus on innovation, Boeing is well placed to lead the aerospace industry into the next era.

Stock Analysis

In this section we will analyze Toyota’s stock to see if it is a good stock to buy or not. Our philosophy is value investing meaning that we try to find good quality companies that are undervalued. However, we will give a holistic overview so all kind of investors with different philosophies can judge the stock for themselves.

Revenue and Profits

Illustration 9 and 10: Revenue of Boeing from 2009 to 2024

As shown in Illustrations 9 and 10, Boeing’s revenue trajectory has had sharp fluctuations rather than steady growth, with a particularly severe decline between 2018 and 2020. After peaking at around USD 101 billion in 2018, revenues plunged to approximately USD 58 billion by 2020, a staggering drop of over 40% in just two years. This steep decline, triggered by the grounding of the 737 MAX and compounded by the COVID-19 pandemic’s impact on global air travel, raising red flags for investors about Boeing’s operational resilience and crisis management.

While Boeing has made progress in recovering since then, revenues have not yet returned to pre-2018 levels as of 2024. The pace of recovery has been gradual, reflecting ongoing efforts to stabilize production, resolve supply chain issues, and rebuild customer confidence. Boeing’s focus on both commercial and defense segments provides some diversification, but its performance remains sensitive to the global aerospace market and regulatory developments.

Overall, Boeing’s financial performance over the past several years reflects a company navigating a complex recovery phase. The revenue volatility underscores the challenges faced during a turbulent period, but also highlights the potential for future growth as commercial aviation rebounds and new aircraft programs come online. For investors, this mixed picture calls for careful monitoring rather than a clear red or green flag.

Illustration 11 and 12: Net Income of Boeing from 2009 to 2024

Net income is a crucial metric to evaluate when determining whether a company is a worthwhile investment. It represents a company’s net profit or loss after accounting for all revenues, income items, and expenses, calculated as Net Income = Revenue – Expenses.

As seen in Illustrations 10 and 11, Boeing’s net income has shown significant volatility, with a sharp decline into negative territory from 2018 to 2020. This drop, driven by the 737 MAX crisis and the pandemic’s impact on air travel, marks a clear red flag, as profits fell even more steeply than revenues.

Although Boeing has made efforts to recover, net income remains inconsistent, reflecting ongoing challenges in production, regulation, and market demand. Unlike companies with steady profit growth, Boeing’s recent earnings instability signals elevated risk for investors focused on financial reliability.

Revenue Breakdown

Illustration 13: Revenue breakdown of Boeing Co,

As shown in Illustration 13, Boeing’s core Commercial Airplanes segment remains its largest revenue contributor, typically accounting for around 40% of total revenue. This includes sales of aircraft such as the 737, 787, and 777 models to global airline customers and leasing firms. While historically a strong growth engine, this segment has experienced significant disruption since 2019 due to the 737 MAX grounding, COVID-19, and ongoing supply chain issues, resulting in elevated costs and production delays.

The Defense, Space & Security division, contributing around 35% of revenue, provides more consistent performance through multi-year government contracts for military aircraft, satellites, and surveillance systems. Boeing Global Services, making up roughly 26% of revenue, generates recurring income from maintenance, spare parts, pilot training, and digital analytics—supporting airline customers through fleet lifecycle services.

Boeing’s main costs that eats up most of it’s revenue is cost of goods sold (COGS) which remains very high, typically representing around 94.7% of revenue, reflecting the capital-intensive nature of aircraft production and frequent cost overruns related to rework and supply constraints. SG&A expenses covers global operations, customer support, and corporate functions while R&D expenses focuses on fuel efficiency, autonomous systems, digital engineering, and sustainable aviation, though these initiatives are still early in commercial impact. Emerging technologies such as space-based systems, electric propulsion, and advanced air mobility are strategically important but currently represent a small share of revenue. These areas are gradually expanding through joint ventures and government partnerships.

Overall, Boeing’s revenue structure reflects both high operating complexity and long-term diversification. While its defense and services businesses offer some financial stability, elevated costs and pressures in the commercial segment pose near-term challenges. The company’s ongoing investment in innovation underscores its long-term vision, but achieving margin recovery will depend on execution, supply chain normalization, and restoring commercial delivery volumes.

Earnings per Share

Illustration 14: Earnings per share for Boeing from 2009 to 2024

Earnings Per Share (EPS) is a key financial metric that measures a company’s profitability on a per-share basis. It indicates how much profit a company generates for each outstanding share of its stock, and is used to assess a company’s financial health, profitability, and potential for growth. In other words this metric can tell us how profitable the business is.

The EPS figure itself isn’t the primary focus for value investors, it can be 0.2 or 10, but what truly matters is the company’s ability to generate consistent earnings growth. A steadily increasing EPS over time signals strong financial health, profitability, and long-term value creation.

Boeing’s earnings per share from 2009 to 2025 shows a sharp decline from 17.85 in 2018 to -20.88 in 2020, marking a significant red flag. This drop was driven by the 737 MAX grounding and the pandemic’s impact on global aviation. While EPS has recovered somewhat in recent years, it remains below pre-crisis levels, reflecting continued cost pressures, supply chain issues, and production delays. The volatility in earnings highlights Boeing’s financial vulnerability during industry shocks and signals ongoing risk. For investors, this uneven trend raises concerns about near-term stability despite the company’s long-term strategic efforts. Furthermore, it had another significant drop from 2023 to 2024. These developments should be closely monitored by potential investors and are clear red flags.

Assets and Liabilities

Illustration 15 and 16: Assets and Liabilities for Boeing from 2009 to 2024

When evaluating a company as a potential investment, understanding its assets and liabilities is crucial. If a local business owner offered to sell their shop to you, one of the first questions. after determining its profitability, would be about its equity and assets. The same principle applies when assessing publicly traded companies like Boeing.

As shown in Illustrations 14 and 15, Boeing’s total assets reached approximately $156 billion in 2024, a figure that reflects the scale of its global operations. However, unlike the steady asset growth seen in some peers, Boeing’s asset base has fluctuated over the past decade due to write-downs, delivery delays, and program-related adjustments. While recent investments in next-generation aircraft and digital systems signal a forward-looking strategy, overall asset growth has been modest and uneven.

At the same time, Boeing’s total liabilities have increased substantially, rising to over $160 billion in 2024. Much of this is tied to debt issued during the pandemic to maintain liquidity and stabilize operations. While some leverage is expected in capital-intensive industries, Boeing’s high debt load combined with continued cash flow pressures raises concerns and big red flags about long-term financial flexibility and resilience. Investors should closely monitor Boeing’s ability to reduce debt and restore balance sheet strength in the coming years.

The critical issue for investors is whether Boeing can return to sustained profitability while managing its obligations. With thin margins and ongoing production costs, the company faces the challenge of generating sufficient free cash flow to reduce its liabilities without sacrificing investment in innovation and quality control. Failure to improve operating efficiency or deliver aircraft at scale could intensify financial strain.

Boeing’s cash on hand in 2024 remains relatively low compared to its long-term debt, which presents a red flag for liquidity. This imbalance could make it more difficult to weather unexpected disruptions or fund strategic initiatives without additional borrowing or asset sales. Investors should keep a close watch on Boeing’s cash generation and working capital management to assess its ability to support operations and repay obligations in the near term.

As seen in Illustration 15, Boeing’s total shareholder equity has turned negative in recent years, meaning its liabilities exceed its assets. This trend is a serious concern, as it indicates erosion of the company’s financial foundation and limited cushion against further losses. Negative equity can restrict financial flexibility and undermine investor confidence, especially if cash flow does not improve. While Boeing retains strong long-term potential in aerospace and defense, rebuilding equity will be essential to restoring investor trust and ensuring long-term financial stability.

Debt to Equity Ratio

Illustration 17 and 18: Debt to Equity ratio for Boeing from 2009 to 2024

The Debt-to-Equity (D/E) ratio is an important financial metric for assessing a company’s financial leverage and risk. It compares the amount of debt a company uses to finance its operations relative to its shareholder equity. A high D/E ratio suggests the company relies more heavily on debt, increasing financial risk, especially during periods of economic stress. In contrast, a lower D/E ratio implies more conservative financing through equity, offering greater financial stability but possibly slower expansion.

Legendary value investor Warren Buffett generally prefers a D/E ratio below 0.5. However, Boeing’s total shareholder equity turned negative in recent years, meaning its liabilities now exceed its assets. As a result, the D/E ratio is no longer a meaningful metric in the traditional sense, it is effectively undefined or extremely high. This situation signals a red flag, as it reflects the long-term financial strain caused by the 737 MAX crisis, pandemic-era losses, and the need for heavy borrowing to sustain operations. Restoring equity and reducing debt will be critical to improving financial health. Until then, the absence of a meaningful D/E ratio highlights the company’s reliance on debt financing and underscores the importance of disciplined cash flow management and margin recovery in the years ahead.

Price to earning ratio (P/E)

Illustration 19 and 20: Price to Earnings ratio for Boeing from 2009 to 2024

For value investors, one of the most critical metrics when evaluating Boeing’s stock is the price-to-earnings (P/E) ratio, as it helps assess whether the company is undervalued or overvalued. Even if a company has a strong brand and global footprint, paying too much for its stock can still result in poor returns. For example, imagine a business that earns $1 million annually, if offered to you for $1, it’s a steal. But if the owner asks $1 trillion, the profitability becomes irrelevant, the price is simply too high. The stock market works the same way: even good companies can be bad investments if bought at inflated prices.

Warren Buffett, a legendary value investor, generally prefers companies with a P/E ratio below 15, viewing them as attractively priced relative to earnings. In Boeing’s case, the situation is more complex. Due to multi-year losses from 2019 to 2021, Boeing’s P/E ratio has either been undefined or exceptionally high during those periods. As earnings have begun to recover, the P/E ratio remains volatile, sensitive to quarterly swings and investor sentiment. As of 2024, Boeing trades at a forward P/E ratio above 40, reflecting high expectations for recovery rather than current earnings strength.

For value investors, this elevated P/E signals caution. While Boeing’s long-term aerospace and defense prospects remain strong, the current valuation suggests that much of the recovery optimism is already priced in. Unless earnings normalize quickly and sustainably, the stock may offer limited margin of safety at current levels.

Price to Book ratio (P/B)

Illustration 21 and 22: Price to book ratio for Boeing from 2009 to 2024

Price-to-book value (P/B ratio) compares a company’s market value to its book value, calculated as total assets minus total liabilities. A low P/B ratio may indicate undervaluation, while a high ratio can signal overvaluation or strong growth expectations. Value investors, including Warren Buffett, often prefer P/B ratios under 1.5, ideally closer to 1.3, when seeking companies trading below their intrinsic asset value.

For Boeing, however, the P/B ratio is no longer meaningful, as the company’s shareholder equity has turned negative in recent years due to accumulated losses and rising liabilities. This means the book value per share is also negative, making the traditional P/B metric undefined.

Rather than suggesting undervaluation, this situation is a red flag, highlighting the weakened state of Boeing’s balance sheet. While Boeing continues to hold strategic value in commercial and defense aerospace, value investors are likely to remain cautious until equity becomes positive again and financial fundamentals stabilize.

Return on Investment (ROI)

Illustration 23 and 24: Return on Investment for Boeing from 2009 to 2024

For value investors, another essential metric when evaluating Boeing’s stock is Return on Investment (ROI), as it shows how efficiently the company uses its capital to generate profits. In simple terms, ROI measures the return earned relative to the capital required to operate the business. A company may have strong revenue, but if it requires heavy capital to generate modest profits, it may not be an efficient investment. For example, if two firms earn the same profit, but one uses half the capital to do so, it’s clearly more efficient. ROI helps investors identify companies that convert capital into returns effectively—a key consideration in capital-intensive industries like aerospace.

Boeing’s ROI has been highly volatile in recent years, and negative during 2017. While ROI has improved as earnings begin to recover, it still lags behind industry expectations. Boeing’s returns have been erratic, raising questions about capital efficiency and long-term value creation. As shown in Illustration 23 and 24, this inconsistent performance reflects the ongoing challenges Boeing faces in restoring operational stability, managing debt, and navigating cost overruns. For long-term investors, this is a cautionary signal, as it suggests that the company has yet to regain full control over its capital deployment. While Boeing remains a leader in aerospace innovation, meaningful improvement in ROI will be key to signaling that the company is delivering sustainable value from its significant investments. A 13% ROI for Boeing in 2024 is a good sign, especially considering its turbulent past few years. It suggests Boeing is becoming more efficient with its capital again. However, it should be assessed alongside other metrics, like cash flow, equity, debt levels, and order backlog, to judge whether the improvement is sustainable and investable.

Dividend

Illustration 25: Dividend Yield and dividend payout ratio from 2005 to 2025 for Boeing

Boeing has historically been a reliable dividend payer, with its annual dividend reaching as high as $2.06 per share in early 2020 and an average dividend yield around 2.5% over the past five years. However, Boeing suspended dividend payments in March 2020 amid financial challenges from the 737 MAX crisis and the COVID-19 pandemic. Since then, no dividends have been issued.

In 2024, Boeing reported a negative earnings per share (EPS) of approximately -$18.36, and while its dividend payout ratio would have been around 48% based on prior earnings patterns, the suspension means the actual payout ratio is effectively zero. This pause in dividends is a red flag for income-focused investors who value steady cash returns. That it has suspended dividends is a big red flag for investors.

Insider Trading

Illustration 26: Recent insider trading at yahoo, gathered from yahoo finance

Recent insider trading activity at Boeing has shown a significant increase in insider selling, which may raise concerns for investors. Between early and mid-May 2025, multiple senior executives, including Boeing’s Executive Vice Presidents and Presidents of major divisions sold substantial amounts of company stock, collectively worth several million dollars. While insider selling can be part of routine financial planning or diversification, the concentrated timing and volume of these sales are noteworthy.

Insider selling at this level can be interpreted as a potential red flag, as it may suggest that insiders have less confidence in the company’s near-term prospects or are taking advantage of current stock prices before possible declines. For value investors, such activity warrants closer scrutiny and signals the importance of monitoring Boeing’s forthcoming earnings results, operational updates, and market conditions.

Other Company Info

Founded in 1916, The Boeing Company is one of the world’s largest and most respected aerospace manufacturers, known for its commercial aircraft, defense systems, and space technologies. As of 2024, Boeing employs approximately 140,000 people globally, reflecting its extensive operations in manufacturing, engineering, research, and services. The company is publicly traded on the New York Stock Exchange (NYSE) under the ticker symbol BA and operates within the Industrials sector, specifically in the Aerospace & Defense industry.

Boeing is headquartered at 100 North Riverside Plaza, Chicago, Illinois, USA. As of 2024, the company has approximately 560 million shares outstanding, with a market capitalization of around $140 billion USD. For more information, visit Boeing’s official website: https://www.boeing.com.